Page 210 - Accountancy_F5

P. 210

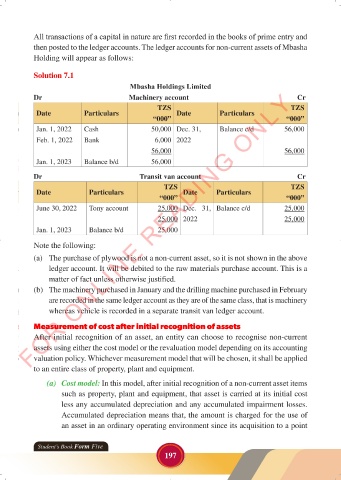

All transactions of a capital in nature are first recorded in the books of prime entry and

then posted to the ledger accounts. The ledger accounts for non-current assets of Mbasha

Holding will appear as follows:

Solution 7.1

Mbasha Holdings Limited

FOR ONLINE READING ONLY

Dr Machinery account Cr

TZS TZS

Date Particulars Date Particulars

“000” “000”

Jan. 1, 2022 Cash 50,000 Dec. 31, Balance c/d

LANGUAGE EDITING

Feb. 1, 2022 Bank 6,000 2022

56,000 56,000

Jan. 1, 2023 Balance b/d 56,000

Dr Transit van account Cr

TZS TZS

Date Particulars Date Particulars

“000” “000”

June 30, 2022 Tony account 25,000 Dec. 31, Balance c/d 25,000

25,000 2022 25,000

Jan. 1, 2023 LANGUAGE EDITING 56,000

25,000

Balance b/d

Note the following:

(a) The purchase of plywood is not a non-current asset, so it is not shown in the above

ledger account. It will be debited to the raw materials purchase account. This is a

matter of fact unless otherwise justified.

(b) The machinery purchased in January and the drilling machine purchased in February

are recorded in the same ledger account as they are of the same class, that is machinery

whereas vehicle is recorded in a separate transit van ledger account.

Measurement of cost after initial recognition of assets

After initial recognition of an asset, an entity can choose to recognise non-current

assets using either the cost model or the revaluation model depending on its accounting

valuation policy. Whichever measurement model that will be chosen, it shall be applied

to an entire class of property, plant and equipment.

(a) Cost model: In this model, after initial recognition of a non-current asset items

such as property, plant and equipment, that asset is carried at its initial cost

less any accumulated depreciation and any accumulated impairment losses.

Accumulated depreciation means that, the amount is charged for the use of

an asset in an ordinary operating environment since its acquisition to a point

Student’s Book Form Five

197

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 197

ACCOUNTANCY_DUMMY_23 JUNE.indd 197 23/06/2024 17:35