Page 94 - Accountancy_F5

P. 94

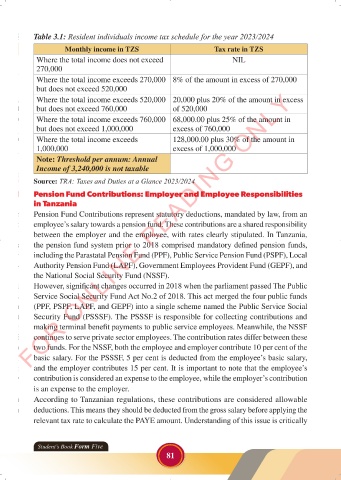

Table 3.1: Resident individuals income tax schedule for the year 2023/2024

Monthly income in TZS Tax rate in TZS

Where the total income does not exceed NIL

270,000

Where the total income exceeds 270,000 8% of the amount in excess of 270,000

but does not exceed 520,000

FOR ONLINE READING ONLY

Where the total income exceeds 520,000 20,000 plus 20% of the amount in excess

but does not exceed 760,000 of 520,000

Where the total income exceeds 760,000 68,000.00 plus 25% of the amount in

LANGUAGE EDITING

but does not exceed 1,000,000 excess of 760,000

Where the total income exceeds 128,000.00 plus 30% of the amount in

LANGUAGE EDITING

1,000,000 excess of 1,000,000

Note: Threshold per annum: Annual

Income of 3,240,000 is not taxable

Source: TRA: Taxes and Duties at a Glance 2023/2024

Pension Fund Contributions: Employer and Employee Responsibilities

in Tanzania

Pension Fund Contributions represent statutory deductions, mandated by law, from an

employee’s salary towards a pension fund. These contributions are a shared responsibility

between the employer and the employee, with rates clearly stipulated. In Tanzania,

the pension fund system prior to 2018 comprised mandatory defined pension funds,

including the Parastatal Pension Fund (PPF), Public Service Pension Fund (PSPF), Local

Authority Pension Fund (LAPF), Government Employees Provident Fund (GEPF), and

the National Social Security Fund (NSSF).

However, significant changes occurred in 2018 when the parliament passed The Public

Service Social Security Fund Act No.2 of 2018. This act merged the four public funds

(PPF, PSPF, LAPF, and GEPF) into a single scheme named the Public Service Social

Security Fund (PSSSF). The PSSSF is responsible for collecting contributions and

making terminal benefit payments to public service employees. Meanwhile, the NSSF

continues to serve private sector employees. The contribution rates differ between these

two funds. For the NSSF, both the employee and employer contribute 10 per cent of the

basic salary. For the PSSSF, 5 per cent is deducted from the employee’s basic salary,

and the employer contributes 15 per cent. It is important to note that the employee’s

contribution is considered an expense to the employee, while the employer’s contribution

is an expense to the employer.

According to Tanzanian regulations, these contributions are considered allowable

deductions. This means they should be deducted from the gross salary before applying the

relevant tax rate to calculate the PAYE amount. Understanding of this issue is critically

Student’s Book Form Five

81

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 81

ACCOUNTANCY_DUMMY_23 JUNE.indd 81 23/06/2024 17:35