Page 133 - Book-keeping for Secondary Schools Student’s Book Form One

P. 133

Trial balance

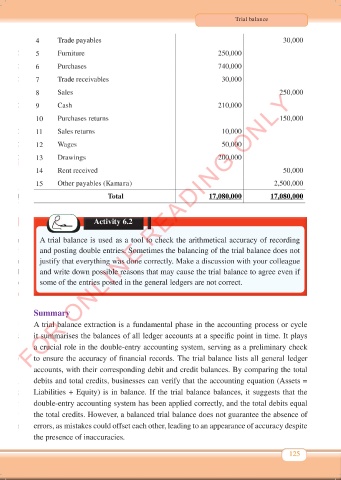

4 Trade payables 30,000

5 Furniture 250,000

6 Purchases 740,000

7 Trade receivables 30,000

FOR ONLINE READING ONLY

8 Sales 250,000

9 Cash 210,000

10 Purchases returns 150,000

11 Sales returns 10,000

12 Wages 50,000

13 Drawings 200,000

14 Rent received 50,000

15 Other payables (Kamara) 2,500,000

Total 17,080,000 17,080,000

Activity 6.2

A trial balance is used as a tool to check the arithmetical accuracy of recording

and posting double entries. Sometimes the balancing of the trial balance does not

justify that everything was done correctly. Make a discussion with your colleague

and write down possible reasons that may cause the trial balance to agree even if

some of the entries posted in the general ledgers are not correct.

Summary

A trial balance extraction is a fundamental phase in the accounting process or cycle

it summarises the balances of all ledger accounts at a specific point in time. It plays

a crucial role in the double-entry accounting system, serving as a preliminary check

to ensure the accuracy of financial records. The trial balance lists all general ledger

accounts, with their corresponding debit and credit balances. By comparing the total

debits and total credits, businesses can verify that the accounting equation (Assets =

Liabilities + Equity) is in balance. If the trial balance balances, it suggests that the

double-entry accounting system has been applied correctly, and the total debits equal

the total credits. However, a balanced trial balance does not guarantee the absence of

errors, as mistakes could offset each other, leading to an appearance of accuracy despite

the presence of inaccuracies.

125

Book Keeping Form 1 New 2024 FINAL.indd 125 18/10/2024 10:14