Page 318 - Agriculture_Form_Three

P. 318

Agriculture for Secondary Schools

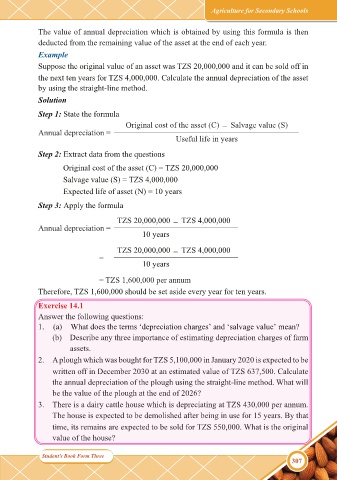

The value of annual depreciation which is obtained by using this formula is then

deducted from the remaining value of the asset at the end of each year.

Example

Suppose the original value of an asset was TZS 20,000,000 and it can be sold off in

the next ten years for TZS 4,000,000. Calculate the annual depreciation of the asset

by using the straight-line method.

Solution

Step 1: State the formula

Original cost of the asset (C) Salvage value (S)

−

Annual depreciation =

Useful life in years

Step 2: Extract data from the questions

Original cost of the asset (C) = TZS 20,000,000

Salvage value (S) = TZS 4,000,000

Expected life of asset (N) = 10 years

Step 3: Apply the formula

TZS 20,000,000 TZS 4,000,000

−

Annual depreciation =

10 years

TZS 20,000,000 TZS 4,000,000

−

=

10 years

= TZS 1,600,000 per annum

Therefore, TZS 1,600,000 should be set aside every year for ten years.

Exercise 14.1

Answer the following questions:

1. (a) What does the terms ‘depreciation chargesʼ and ‘salvage valueʼ mean?

(b) Describe any three importance of estimating depreciation charges of farm

assets.

2. A plough which was bought for TZS 5,100,000 in January 2020 is expected to be

written off in December 2030 at an estimated value of TZS 637,500. Calculate

the annual depreciation of the plough using the straight-line method. What will

be the value of the plough at the end of 2026?

3. There is a dairy cattle house which is depreciating at TZS 430,000 per annum.

The house is expected to be demolished after being in use for 15 years. By that

time, its remains are expected to be sold for TZS 550,000. What is the original

value of the house?

Student’

Student’s Book Form Twos Book Form Three

307

10/01/2025 12:32

AGRICULTURE FORM 3 9.11.2022.indd 307

AGRICULTURE FORM 3 9.11.2022.indd 307 10/01/2025 12:32