Page 118 - Accountancy_F5

P. 118

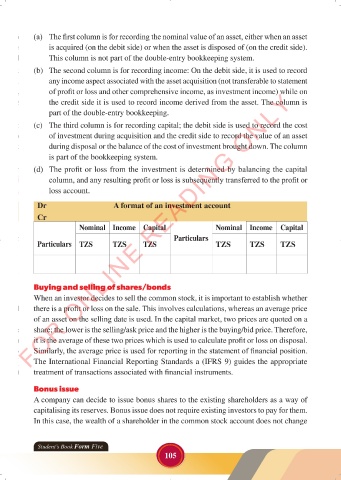

(a) The first column is for recording the nominal value of an asset, either when an asset

is acquired (on the debit side) or when the asset is disposed of (on the credit side).

This column is not part of the double-entry bookkeeping system.

(b) The second column is for recording income: On the debit side, it is used to record

any income aspect associated with the asset acquisition (not transferable to statement

FOR ONLINE READING ONLY

of profit or loss and other comprehensive income, as investment income) while on

the credit side it is used to record income derived from the asset. The column is

part of the double-entry bookkeeping.

LANGUAGE EDITING

(c) The third column is for recording capital; the debit side is used to record the cost

of investment during acquisition and the credit side to record the value of an asset

LANGUAGE EDITING

during disposal or the balance of the cost of investment brought down. The column

is part of the bookkeeping system.

(d) The profit or loss from the investment is determined by balancing the capital

column, and any resulting profit or loss is subsequently transferred to the profit or

loss account.

Dr A format of an investment account

Cr

Nominal Income Capital Nominal Income Capital

Particulars

Particulars TZS TZS TZS TZS TZS TZS

Buying and selling of shares/bonds

When an investor decides to sell the common stock, it is important to establish whether

there is a profit or loss on the sale. This involves calculations, whereas an average price

of an asset on the selling date is used. In the capital market, two prices are quoted on a

share; the lower is the selling/ask price and the higher is the buying/bid price. Therefore,

it is the average of these two prices which is used to calculate profit or loss on disposal.

Similarly, the average price is used for reporting in the statement of financial position.

The International Financial Reporting Standards a (IFRS 9) guides the appropriate

treatment of transactions associated with financial instruments.

Bonus issue

A company can decide to issue bonus shares to the existing shareholders as a way of

capitalising its reserves. Bonus issue does not require existing investors to pay for them.

In this case, the wealth of a shareholder in the common stock account does not change

Student’s Book Form Five

105

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 105 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 105