Page 124 - Accountancy_F5

P. 124

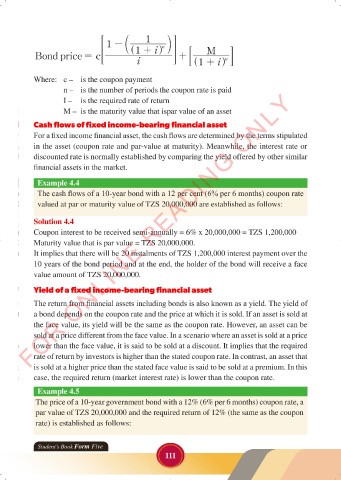

1

1 - c n m

> ^ 1 + ih H M

Bond price= c + ; n E

i ^ 1 + ih

Where: c – is the coupon payment

n – is the number of periods the coupon rate is paid

FOR ONLINE READING ONLY

I – is the required rate of return

M – is the maturity value that ispar value of an asset

Cash flows of fixed income-bearing financial asset

For a fixed income financial asset, the cash flows are determined by the terms stipulated

LANGUAGE EDITING

in the asset (coupon rate and par-value at maturity). Meanwhile, the interest rate or

discounted rate is normally established by comparing the yield offered by other similar

financial assets in the market.

Example 4.4

The cash flows of a 10-year bond with a 12 per cent (6% per 6 months) coupon rate

valued at par or maturity value of TZS 20,000,000 are established as follows:

Solution 4.4 LANGUAGE EDITING

Coupon interest to be received semi-annually = 6% x 20,000,000 = TZS 1,200,000

Maturity value that is par value = TZS 20,000,000.

It implies that there will be 20 instalments of TZS 1,200,000 interest payment over the

10 years of the bond period and at the end, the holder of the bond will receive a face

value amount of TZS 20,000,000.

Yield of a fixed income-bearing financial asset

The return from financial assets including bonds is also known as a yield. The yield of

a bond depends on the coupon rate and the price at which it is sold. If an asset is sold at

the face value, its yield will be the same as the coupon rate. However, an asset can be

sold at a price different from the face value. In a scenario where an asset is sold at a price

lower than the face value, it is said to be sold at a discount. It implies that the required

rate of return by investors is higher than the stated coupon rate. In contrast, an asset that

is sold at a higher price than the stated face value is said to be sold at a premium. In this

case, the required return (market interest rate) is lower than the coupon rate.

Example 4.5

The price of a 10-year government bond with a 12% (6% per 6 months) coupon rate, a

par value of TZS 20,000,000 and the required return of 12% (the same as the coupon

rate) is established as follows:

Student’s Book Form Five

111

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 111

ACCOUNTANCY_DUMMY_23 JUNE.indd 111 23/06/2024 17:35