Page 128 - Accountancy_F5

P. 128

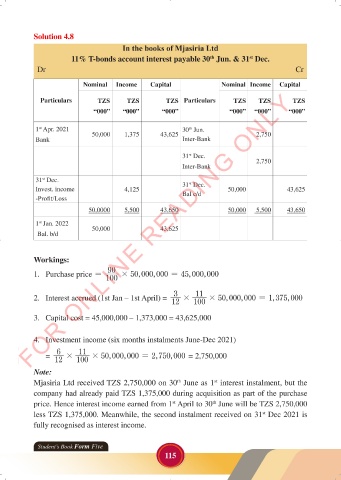

Solution 4.8

In the books of Mjasiria Ltd

11% T-bonds account interest payable 30 Jun. & 31 Dec.

st

th

Dr Cr

Nominal Income Capital Nominal Income Capital

FOR ONLINE READING ONLY

Particulars TZS TZS TZS Particulars TZS TZS TZS

“000” “000” “000” “000” “000” “000”

1 Apr. 2021 50,000 1,375 43,625 30 Jun. 2,750

st

th

LANGUAGE EDITING

Bank Inter-Bank

31 Dec.

st

2,750

Inter-Bank

31 Dec. 31 Dec.

st

st

Invest. income 4,125 Bal c/d 50,000 43,625

-Profit/Loss

50,0000 5,500 43,650 50,000 5,500 43,650

1 Jan. 2022 LANGUAGE EDITING

st

50,000

43,625

Bal. b/d

Workings:

90

1. Purchase price = # 50 ,000 000 = 45 ,000 000

,

,

100

2. Interest accrued (1st Jan – 1st April) = 3 # 11 # 50 ,000 000 = , 1 375 000

,

,

12 100

3. Capital cost = 45,000,000 – 1,373,000 = 43,625,000

4. Investment income (six months instalments June-Dec 2021)

= 6 # 11 # 50 ,000 000 = , 2 750 000 = 2,750,000

,

,

12 100

Note:

Mjasiria Ltd received TZS 2,750,000 on 30 June as 1 interest instalment, but the

st

th

company had already paid TZS 1,375,000 during acquisition as part of the purchase

price. Hence interest income earned from 1 April to 30 June will be TZS 2,750,000

th

st

less TZS 1,375,000. Meanwhile, the second instalment received on 31 Dec 2021 is

st

fully recognised as interest income.

Student’s Book Form Five

115

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 115 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 115