Page 131 - Accountancy_F5

P. 131

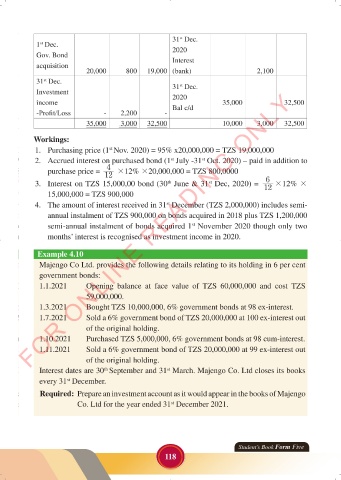

31 Dec.

st

1 Dec. 2020

st

Gov. Bond Interest

acquisition

20,000 800 19,000 (bank) 2,100

31 Dec. 31 Dec.

st

st

FOR ONLINE READING ONLY

Investment 2020

income Bal c/d 35,000 32,500

-Profit/Loss - 2,200 -

35,000 3,000 32,500 10,000 3,000 32,500

Workings:

LANGUAGE EDITING

1. Purchasing price (1 Nov. 2020) = 95% x20,000,000 = TZS 19,000,000

st

2. Accrued interest on purchased bond (1 July -31 Oct. 2020) – paid in addition to

st

st

4

purchase price = 12 #12% #20,000,000 = TZS 800,0000

6

3. Interest on TZS 15,000,00 bond (30 June & 31 Dec, 2020) = 12 #12% #

th

st

15,000,000 = TZS 900,000

4. The amount of interest received in 31 December (TZS 2,000,000) includes semi-

st

annual instalment of TZS 900,000 on bonds acquired in 2018 plus TZS 1,200,000

semi-annual instalment of bonds acquired 1 November 2020 though only two

st

months’ interest is recognised as investment income in 2020.

Example 4.10

Majengo Co Ltd. provides the following details relating to its holding in 6 per cent

government bonds:

1.1.2021 Opening balance at face value of TZS 60,000,000 and cost TZS

59,000,000.

1.3.2021 Bought TZS 10,000,000, 6% government bonds at 98 ex-interest.

1.7.2021 Sold a 6% government bond of TZS 20,000,000 at 100 ex-interest out

of the original holding.

1.10.2021 Purchased TZS 5,000,000, 6% government bonds at 98 cum-interest.

1.11.2021 Sold a 6% government bond of TZS 20,000,000 at 99 ex-interest out

of the original holding.

Interest dates are 30 September and 31 March. Majengo Co. Ltd closes its books

st

th

every 31 December.

st

Required: Prepare an investment account as it would appear in the books of Majengo

Co. Ltd for the year ended 31 December 2021.

st

Student’s Book Form Five

118

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 118 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 118