Page 153 - Accountancy_F5

P. 153

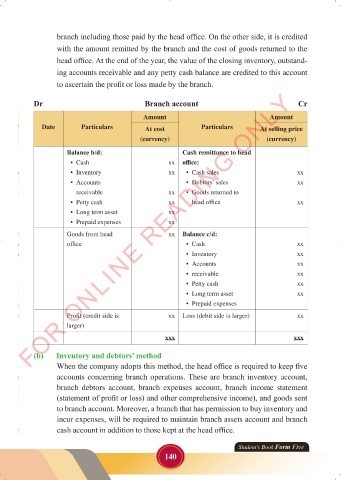

branch including those paid by the head office. On the other side, it is credited

with the amount remitted by the branch and the cost of goods returned to the

head office. At the end of the year, the value of the closing inventory, outstand-

ing accounts receivable and any petty cash balance are credited to this account

to ascertain the profit or loss made by the branch.

FOR ONLINE READING ONLY

Dr Branch account Cr

Amount Amount

Date Particulars At cost Particulars At selling price

LANGUAGE EDITING

(currency) (currency)

Balance b/d: Cash remittance to head

• Cash xx office:

• Inventory xx • Cash sales xx

• Accounts • Debtors’ sales xx

receivable xx • Goods returned to

• Petty cash xx head office xx

• Long term asset xx

• Prepaid expenses xx

Goods from head xx Balance c/d:

office • Cash xx

• Inventory xx

• Accounts xx

• receivable xx

• Petty cash xx

• Long term asset xx

• Prepaid expenses

Profit (credit side is xx Loss (debit side is larger) xx

larger)

xxx xxx

(b) Inventory and debtors’ method

When the company adopts this method, the head office is required to keep five

accounts concerning branch operations. These are branch inventory account,

branch debtors account, branch expenses account, branch income statement

(statement of profit or loss) and other comprehensive income), and goods sent

to branch account. Moreover, a branch that has permission to buy inventory and

incur expenses, will be required to maintain branch assets account and branch

cash account in addition to those kept at the head office.

Student’s Book Form Five

140

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 140

ACCOUNTANCY_DUMMY_23 JUNE.indd 140 23/06/2024 17:35