Page 152 - Accountancy_F5

P. 152

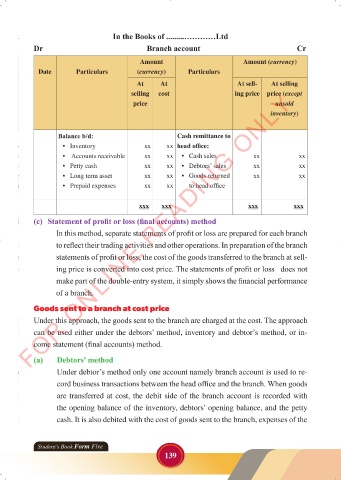

In the Books of .........…………Ltd

Dr Branch account Cr

Amount Amount (currency)

Date Particulars (currency) Particulars

At At At sell- At selling

FOR ONLINE READING ONLY

selling cost ing price price (except

price unsold

inventory)

LANGUAGE EDITING

Balance b/d: Cash remittance to

LANGUAGE EDITING

• Inventory xx xx head office:

• Accounts receivable xx xx • Cash sales xx xx

• Petty cash xx xx • Debtors’ sales xx xx

• Long term asset xx xx • Goods returned xx xx

• Prepaid expenses xx xx to head office

xxx xxx xxx xxx

(c) Statement of profit or loss (final accounts) method

In this method, separate statements of profit or loss are prepared for each branch

to reflect their trading activities and other operations. In preparation of the branch

statements of profit or loss, the cost of the goods transferred to the branch at sell-

ing price is converted into cost price. The statements of profit or loss does not

make part of the double-entry system, it simply shows the financial performance

of a branch.

Goods sent to a branch at cost price

Under this approach, the goods sent to the branch are charged at the cost. The approach

can be used either under the debtors’ method, inventory and debtor’s method, or in-

come statement (final accounts) method.

(a) Debtors’ method

Under debtor’s method only one account namely branch account is used to re-

cord business transactions between the head office and the branch. When goods

are transferred at cost, the debit side of the branch account is recorded with

the opening balance of the inventory, debtors’ opening balance, and the petty

cash. It is also debited with the cost of goods sent to the branch, expenses of the

Student’s Book Form Five

139

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 139 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 139