Page 147 - Accountancy_F5

P. 147

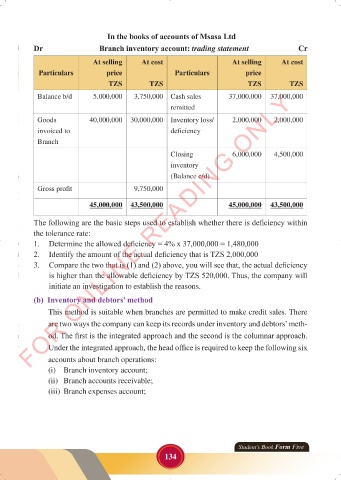

In the books of accounts of Msasa Ltd

Dr Branch inventory account: trading statement Cr

At selling At cost At selling At cost

Particulars price Particulars price

TZS TZS TZS TZS

FOR ONLINE READING ONLY

Balance b/d 5,000,000 3,750,000 Cash sales 37,000,000 37,000,000

remitted

Goods 40,000,000 30,000,000 Inventory loss/ 2,000,000 2,000,000

invoiced to deficiency

LANGUAGE EDITING

Branch

Closing 6,000,000 4,500,000

inventory

(Balance c/d)

Gross profit 9,750,000

45,000,000 43,500,000 45,000,000 43,500,000

The following are the basic steps used to establish whether there is deficiency within

the tolerance rate:

1. Determine the allowed deficiency = 4% x 37,000,000 = 1,480,000

2. Identify the amount of the actual deficiency that is TZS 2,000,000

3. Compare the two that is (1) and (2) above, you will see that, the actual deficiency

is higher than the allowable deficiency by TZS 520,000. Thus, the company will

initiate an investigation to establish the reasons.

(b) Inventory and debtors’ method

This method is suitable when branches are permitted to make credit sales. There

are two ways the company can keep its records under inventory and debtors’ meth-

od. The first is the integrated approach and the second is the columnar approach.

Under the integrated approach, the head office is required to keep the following six

accounts about branch operations:

(i) Branch inventory account;

(ii) Branch accounts receivable;

(iii) Branch expenses account;

Student’s Book Form Five

134

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 134

ACCOUNTANCY_DUMMY_23 JUNE.indd 134 23/06/2024 17:35