Page 160 - Accountancy_F5

P. 160

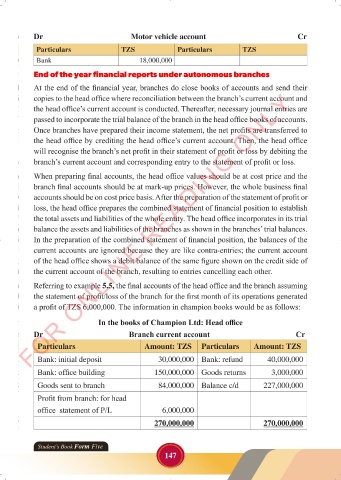

Dr Motor vehicle account Cr

Particulars TZS Particulars TZS

Bank 18,000,000

End of the year financial reports under autonomous branches

At the end of the financial year, branches do close books of accounts and send their

FOR ONLINE READING ONLY

copies to the head office where reconciliation between the branch’s current account and

the head office’s current account is conducted. Thereafter, necessary journal entries are

passed to incorporate the trial balance of the branch in the head office books of accounts.

LANGUAGE EDITING

Once branches have prepared their income statement, the net profits are transferred to

LANGUAGE EDITING

the head office by crediting the head office’s current account. Then, the head office

will recognise the branch’s net profit in their statement of profit or loss by debiting the

branch’s current account and corresponding entry to the statement of profit or loss.

When preparing final accounts, the head office values should be at cost price and the

branch final accounts should be at mark-up prices. However, the whole business final

accounts should be on cost price basis. After the preparation of the statement of profit or

loss, the head office prepares the combined statement of financial position to establish

the total assets and liabilities of the whole entity. The head office incorporates in its trial

balance the assets and liabilities of the branches as shown in the branches’ trial balances.

In the preparation of the combined statement of financial position, the balances of the

current accounts are ignored because they are like contra-entries; the current account

of the head office shows a debit balance of the same figure shown on the credit side of

the current account of the branch, resulting to entries cancelling each other.

Referring to example 5.5, the final accounts of the head office and the branch assuming

the statement of profit/loss of the branch for the first month of its operations generated

a profit of TZS 6,000,000. The information in champion books would be as follows:

In the books of Champion Ltd: Head office

Dr Branch current account Cr

Particulars Amount: TZS Particulars Amount: TZS

Bank: initial deposit 30,000,000 Bank: refund 40,000,000

Bank: office building 150,000,000 Goods returns 3,000,000

Goods sent to branch 84,000,000 Balance c/d 227,000,000

Profit from branch: for head

office statement of P/L 6,000,000

270,000,000 270,000,000

Student’s Book Form Five

147

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 147

ACCOUNTANCY_DUMMY_23 JUNE.indd 147 23/06/2024 17:35