Page 171 - Accountancy_F5

P. 171

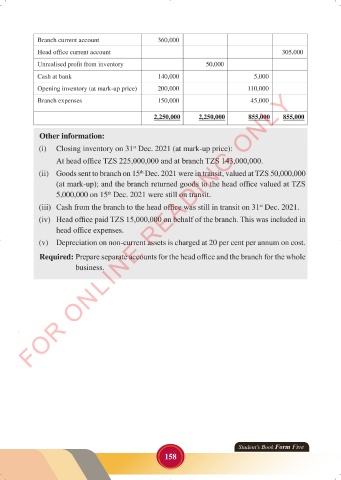

Branch current account 360,000

Head office current account 305,000

Unrealised profit from inventory 50,000

Cash at bank 140,000 5,000

Opening inventory (at mark-up price) 200,000 110,000

FOR ONLINE READING ONLY

Branch expenses 150,000 45,000

2,250,000 2,250,000 855,000 855,000

Other information:

LANGUAGE EDITING

(i) Closing inventory on 31 Dec. 2021 (at mark-up price):

st

At head office TZS 225,000,000 and at branch TZS 143,000,000.

(ii) Goods sent to branch on 15 Dec. 2021 were in transit, valued at TZS 50,000,000

th

(at mark-up); and the branch returned goods to the head office valued at TZS

5,000,000 on 15 Dec. 2021 were still on transit.

th

(iii) Cash from the branch to the head office was still in transit on 31 Dec. 2021.

st

(iv) Head office paid TZS 15,000,000 on behalf of the branch. This was included in

head office expenses.

(v) Depreciation on non-current assets is charged at 20 per cent per annum on cost.

Required: Prepare separate accounts for the head office and the branch for the whole

business.

Student’s Book Form Five

158

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 158 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 158