Page 166 - Accountancy_F5

P. 166

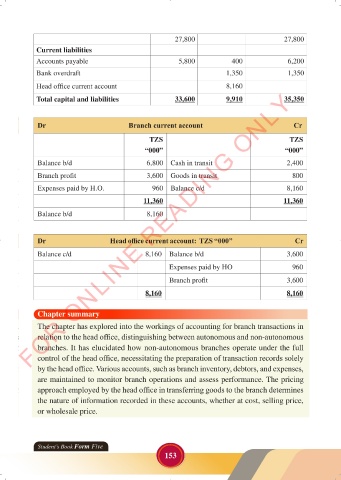

27,800 27,800

Current liabilities

Accounts payable 5,800 400 6,200

Bank overdraft 1,350 1,350

Head office current account 8,160

FOR ONLINE READING ONLY

Total capital and liabilities 33,600 9,910 35,350

Dr Branch current account Cr

TZS TZS

LANGUAGE EDITING

“000” “000”

Balance b/d 6,800 Cash in transit 2,400

Branch profit 3,600 Goods in transit 800

Expenses paid by H.O. 960 Balance c/d 8,160

11,360 11,360

8,160

Balance b/d LANGUAGE EDITING

Dr Head office current account: TZS “000” Cr

Balance c/d 8,160 Balance b/d 3,600

Expenses paid by HO 960

Branch profit 3,600

8,160 8,160

Chapter summary

The chapter has explored into the workings of accounting for branch transactions in

relation to the head office, distinguishing between autonomous and non-autonomous

branches. It has elucidated how non-autonomous branches operate under the full

control of the head office, necessitating the preparation of transaction records solely

by the head office. Various accounts, such as branch inventory, debtors, and expenses,

are maintained to monitor branch operations and assess performance. The pricing

approach employed by the head office in transferring goods to the branch determines

the nature of information recorded in these accounts, whether at cost, selling price,

or wholesale price.

Student’s Book Form Five

153

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 153 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 153