Page 177 - Accountancy_F5

P. 177

the stage of surplus is reached, where he can start recovering the excess over minimum

rent. Short workings can only be recouped from the transactions relating to future royalty

payments only, not backward. Depending on the terms of the royalty contract, the lessee

can start paying for the actual royalty after full or partial recovery of short workings.

Rights of recoupment

FOR ONLINE READING ONLY

Right to recoupment in any royalty agreement can either be fixed right or floating right: -

Fixed right: The lessee has the right to recoup short workings for a fixed time period. In

this case the lessor agrees to compensate the lessee for the losses incurred in the previous

years, by allowing him to recover the difference between actual royalty and minimum

rent for a fixed number of years. For example, the lessor may agree to compensate the

LANGUAGE EDITING

lessee for the short workings only during the first five years, after which any balance of

short workings not recouped will be transferred to the statement of profit or loss as an

expense to the lessee and an income to the lessor.

Floating right: In this case, the lessee has a right to recover the short workings of any

year during the next agreed number of years, following the payment of short workings.

This means the short workings of each year if not recovered, will be carried forward not

further than the next agreed number of years. For example, if the recoverable agreed

period is two years, short workings of the first year can be recouped in the second and/

or third year. Similarly, short workings of the fifth year, can be recouped during the

sixth year and/or seventh year. If it is not possible to recoup the short workings during

the agreed period, the short workings not recouped will be transferred to statement of

profit or loss as an expense to the lessee and an income to the lessor.

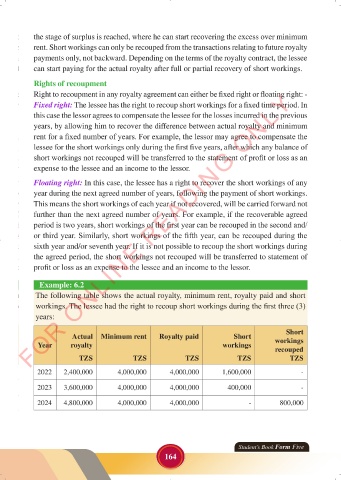

Example: 6.2

The following table shows the actual royalty, minimum rent, royalty paid and short

workings. The lessee had the right to recoup short workings during the first three (3)

years:

Short

Actual Minimum rent Royalty paid Short

Year royalty workings workings

recouped

TZS TZS TZS TZS TZS

2022 2,400,000 4,000,000 4,000,000 1,600,000 -

2023 3,600,000 4,000,000 4,000,000 400,000 -

2024 4,800,000 4,000,000 4,000,000 - 800,000

Student’s Book Form Five

164

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 164

ACCOUNTANCY_DUMMY_23 JUNE.indd 164 23/06/2024 17:35