Page 180 - Accountancy_F5

P. 180

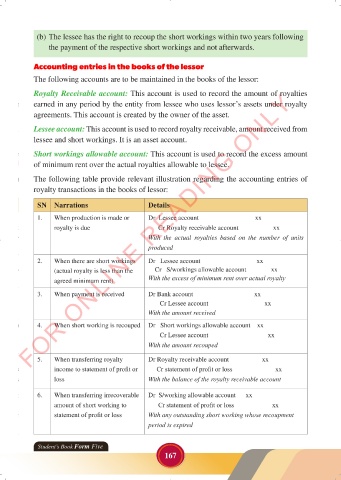

(b) The lessee has the right to recoup the short workings within two years following

the payment of the respective short workings and not afterwards.

Accounting entries in the books of the lessor

The following accounts are to be maintained in the books of the lessor:

FOR ONLINE READING ONLY

Royalty Receivable account: This account is used to record the amount of royalties

earned in any period by the entity from lessee who uses lessor’s assets under royalty

agreements. This account is created by the owner of the asset.

LANGUAGE EDITING

Lessee account: This account is used to record royalty receivable, amount received from

LANGUAGE EDITING

lessee and short workings. It is an asset account.

Short workings allowable account: This account is used to record the excess amount

of minimum rent over the actual royalties allowable to lessee.

The following table provide relevant illustration regarding the accounting entries of

royalty transactions in the books of lessor:

SN Narrations Details

1. When production is made or Dr Lessee account xx

royalty is due Cr Royalty receivable account xx

With the actual royalties based on the number of units

produced

2. When there are short workings Dr Lessee account xx

(actual royalty is less than the Cr S/workings allowable account xx

agreed minimum rent) With the excess of minimum rent over actual royalty

3. When payment is received Dr Bank account xx

Cr Lessee account xx

With the amount received

4. When short working is recouped Dr Short workings allowable account xx

Cr Lessee account xx

With the amount recouped

5. When transferring royalty Dr Royalty receivable account xx

income to statement of profit or Cr statement of profit or loss xx

loss With the balance of the royalty receivable account

6. When transferring irrecoverable Dr S/working allowable account xx

amount of short working to Cr statement of profit or loss xx

statement of profit or loss With any outstanding short working whose recoupment

period is expired

Student’s Book Form Five

167

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 167

ACCOUNTANCY_DUMMY_23 JUNE.indd 167 23/06/2024 17:35