Page 183 - Accountancy_F5

P. 183

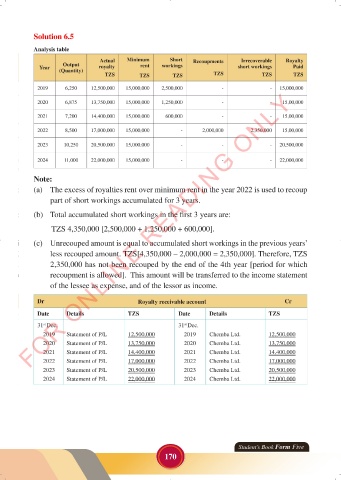

Solution 6.5

Analysis table

Actual Minimum Short Recoupments Irrecoverable Royalty

Output

Year (Quantity) royalty rent workings short workings Paid

TZS TZS TZS TZS TZS TZS

2019 6,250 12,500,000 15,000,000 2,500,000 - - 15,000,000

FOR ONLINE READING ONLY

2020 6,875 13,750,000 15,000,000 1,250,000 - - 15,00,000

2021 7,200 14,400,000 15,000,000 600,000 - - 15,00,000

2022 8,500 17,000,000 15,000,000 - 2,000,000 2,350,000 15,00,000

LANGUAGE EDITING

2023 10,250 20,500,000 15,000,000 - - - 20,500,000

2024 11,000 22,000,000 15,000,000 - - - 22,000,000

Note:

(a) The excess of royalties rent over minimum rent in the year 2022 is used to recoup

part of short workings accumulated for 3 years.

(b) Total accumulated short workings in the first 3 years are:

TZS 4,350,000 [2,500,000 + 1,250,000 + 600,000].

(c) Unrecouped amount is equal to accumulated short workings in the previous years’

less recouped amount. TZS[4,350,000 – 2,000,000 = 2,350,000]. Therefore, TZS

2,350,000 has not been recouped by the end of the 4th year [period for which

recoupment is allowed]. This amount will be transferred to the income statement

of the lessee as expense, and of the lessor as income.

Dr Royalty receivable account Cr

Date Details TZS Date Details TZS

31 Dec. 31 Dec.

st

st

2019 Statement of P/L 12,500,000 2019 Chemba Ltd. 12,500,000

2020 Statement of P/L 13,750,000 2020 Chemba Ltd. 13,750,000

2021 Statement of P/L 14,400,000 2021 Chemba Ltd. 14,400,000

2022 Statement of P/L 17,000,000 2022 Chemba Ltd. 17,000,000

2023 Statement of P/L 20,500,000 2023 Chemba Ltd. 20,500,000

2024 Statement of P/L 22,000,000 2024 Chemba Ltd. 22,000,000

Student’s Book Form Five

170

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 170 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 170