Page 22 - Accountancy_F5

P. 22

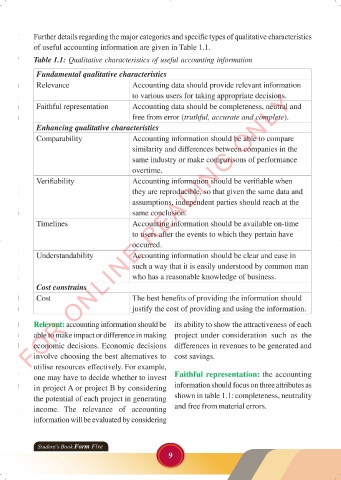

Further details regarding the major categories and specific types of qualitative characteristics

of useful accounting information are given in Table 1.1.

Table 1.1: Qualitative characteristics of useful accounting information

Fundamental qualitative characteristics

Relevance Accounting data should provide relevant information

FOR ONLINE READING ONLY

to various users for taking appropriate decisions.

Faithful representation Accounting data should be completeness, neutral and

free from error (truthful, accurate and complete).

Enhancing qualitative characteristics

Comparability Accounting information should be able to compare

LANGUAGE EDITING

similarity and differences between companies in the

same industry or make comparisons of performance

overtime.

Verifiability Accounting information should be verifiable when

they are reproducible, so that given the same data and

assumptions, independent parties should reach at the

same conclusion.

Timelines LANGUAGE EDITING

Accounting information should be available on-time

to users after the events to which they pertain have

occurred.

Understandability Accounting information should be clear and ease in

such a way that it is easily understood by common man

who has a reasonable knowledge of business.

Cost constrains

Cost The best benefits of providing the information should

justify the cost of providing and using the information.

Relevant: accounting information should be its ability to show the attractiveness of each

able to make impact or difference in making project under consideration such as the

economic decisions. Economic decisions differences in revenues to be generated and

involve choosing the best alternatives to cost savings.

utilise resources effectively. For example,

one may have to decide whether to invest Faithful representation: the accounting

in project A or project B by considering information should focus on three attributes as

the potential of each project in generating shown in table 1.1: completeness, neutrality

income. The relevance of accounting and free from material errors.

information will be evaluated by considering

Student’s Book Form Five

9

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 9 23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 9