Page 25 - Accountancy_F5

P. 25

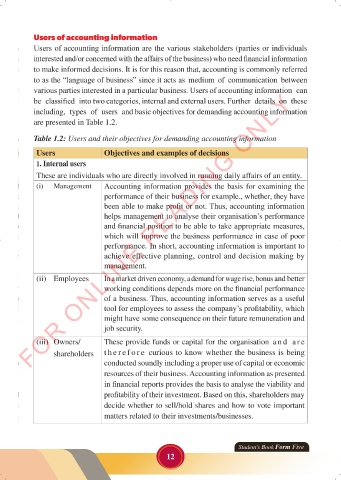

Users of accounting information

Users of accounting information are the various stakeholders (parties or individuals

interested and/or concerned with the affairs of the business) who need financial information

to make informed decisions. It is for this reason that, accounting is commonly referred

to as the “language of business” since it acts as medium of communication between

various parties interested in a particular business. Users of accounting information can

FOR ONLINE READING ONLY

be classified into two categories, internal and external users. Further details on these

including, types of users and basic objectives for demanding accounting information

are presented in Table 1.2.

Table 1.2: Users and their objectives for demanding accounting information

LANGUAGE EDITING

Users Objectives and examples of decisions

1. Internal users

These are individuals who are directly involved in running daily affairs of an entity.

(i) Management Accounting information provides the basis for examining the

performance of their business for example., whether, they have

been able to make profit or not. Thus, accounting information

helps management to analyse their organisation’s performance

and financial position to be able to take appropriate measures,

which will improve the business performance in case of poor

performance. In short, accounting information is important to

achieve effective planning, control and decision making by

management.

(ii) Employees In a market driven economy, a demand for wage rise, bonus and better

working conditions depends more on the financial performance

of a business. Thus, accounting information serves as a useful

tool for employees to assess the company’s profitability, which

might have some consequence on their future remuneration and

job security.

(iii) Owners/ These provide funds or capital for the organisation a n d a r e

shareholders t h e r e f o r e curious to know whether the business is being

conducted soundly including a proper use of capital or economic

resources of their business. Accounting information as presented

in financial reports provides the basis to analyse the viability and

profitability of their investment. Based on this, shareholders may

decide whether to sell/hold shares and how to vote important

matters related to their investments/businesses.

Student’s Book Form Five

12

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 12

ACCOUNTANCY_DUMMY_23 JUNE.indd 12 23/06/2024 17:34