Page 287 - Accountancy_F5

P. 287

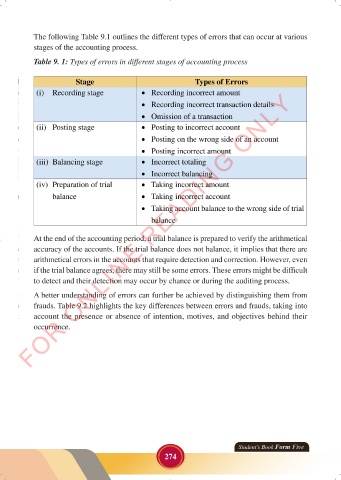

The following Table 9.1 outlines the different types of errors that can occur at various

stages of the accounting process.

Table 9. 1: Types of errors in different stages of accounting process

Stage Types of Errors

FOR ONLINE READING ONLY

(i) Recording stage • Recording incorrect amount

• Recording incorrect transaction details

• Omission of a transaction

(ii) Posting stage • Posting to incorrect account

• Posting on the wrong side of an account

LANGUAGE EDITING

• Posting incorrect amount

(iii) Balancing stage • Incorrect totaling

• Incorrect balancing

(iv) Preparation of trial • Taking incorrect amount

balance • Taking incorrect account

• Taking account balance to the wrong side of trial

balance

At the end of the accounting period, a trial balance is prepared to verify the arithmetical

accuracy of the accounts. If the trial balance does not balance, it implies that there are

arithmetical errors in the accounts that require detection and correction. However, even

if the trial balance agrees, there may still be some errors. These errors might be difficult

to detect and their detection may occur by chance or during the auditing process.

A better understanding of errors can further be achieved by distinguishing them from

frauds. Table 9.2 highlights the key differences between errors and frauds, taking into

account the presence or absence of intention, motives, and objectives behind their

occurrence.

Student’s Book Form Five

274

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 274 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 274