Page 288 - Accountancy_F5

P. 288

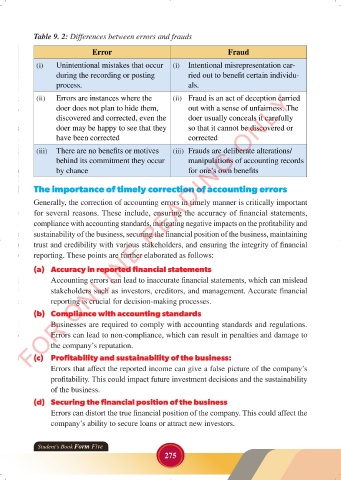

Table 9. 2: Differences between errors and frauds

Error Fraud

(i) Unintentional mistakes that occur (i) Intentional misrepresentation car-

during the recording or posting ried out to benefit certain individu-

process. als.

FOR ONLINE READING ONLY

(ii) Errors are instances where the (ii) Fraud is an act of deception carried

doer does not plan to hide them, out with a sense of unfairness. The

discovered and corrected, even the doer usually conceals it carefully

LANGUAGE EDITING

doer may be happy to see that they so that it cannot be discovered or

have been corrected corrected

LANGUAGE EDITING

(iii) There are no benefits or motives (iii) Frauds are deliberate alterations/

behind its commitment they occur manipulations of accounting records

by chance for one’s own benefits

The importance of timely correction of accounting errors

Generally, the correction of accounting errors in timely manner is critically important

for several reasons. These include, ensuring the accuracy of financial statements,

compliance with accounting standards, mitigating negative impacts on the profitability and

sustainability of the business, securing the financial position of the business, maintaining

trust and credibility with various stakeholders, and ensuring the integrity of financial

reporting. These points are further elaborated as follows:

(a) Accuracy in reported financial statements

Accounting errors can lead to inaccurate financial statements, which can mislead

stakeholders such as investors, creditors, and management. Accurate financial

reporting is crucial for decision-making processes.

(b) Compliance with accounting standards

Businesses are required to comply with accounting standards and regulations.

Errors can lead to non-compliance, which can result in penalties and damage to

the company’s reputation.

(c) Profitability and sustainability of the business:

Errors that affect the reported income can give a false picture of the company’s

profitability. This could impact future investment decisions and the sustainability

of the business.

(d) Securing the financial position of the business

Errors can distort the true financial position of the company. This could affect the

company’s ability to secure loans or attract new investors.

Student’s Book Form Five

275

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 275 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 275