Page 293 - Accountancy_F5

P. 293

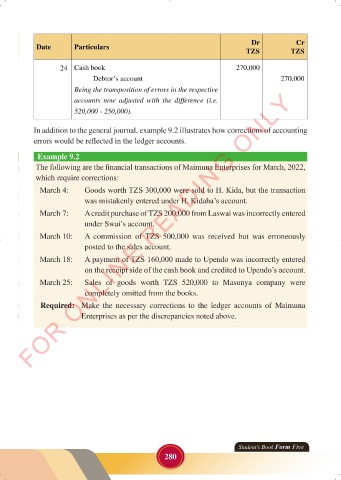

Dr Cr

Date Particulars

TZS TZS

24 Cash book 270,000

Debtor’s account 270,000

Being the transposition of errors in the respective

FOR ONLINE READING ONLY

accounts now adjusted with the difference (i.e.

520,000 - 250,000).

In addition to the general journal, example 9.2 illustrates how corrections of accounting

LANGUAGE EDITING

errors would be reflected in the ledger accounts.

Example 9.2

The following are the financial transactions of Maimuna Enterprises for March, 2022,

which require corrections:

March 4: Goods worth TZS 300,000 were sold to H. Kida, but the transaction

was mistakenly entered under H. Kidaha’s account.

March 7: A credit purchase of TZS 200,000 from Laswai was incorrectly entered

under Swai’s account.

March 10: A commission of TZS 500,000 was received but was erroneously

posted to the sales account.

March 18: A payment of TZS 160,000 made to Upendo was incorrectly entered

on the receipt side of the cash book and credited to Upendo’s account.

March 25: Sales of goods worth TZS 520,000 to Masunya company were

completely omitted from the books.

Required: Make the necessary corrections to the ledger accounts of Maimuna

Enterprises as per the discrepancies noted above.

Student’s Book Form Five

280

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 280 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 280