Page 74 - Accountancy_F5

P. 74

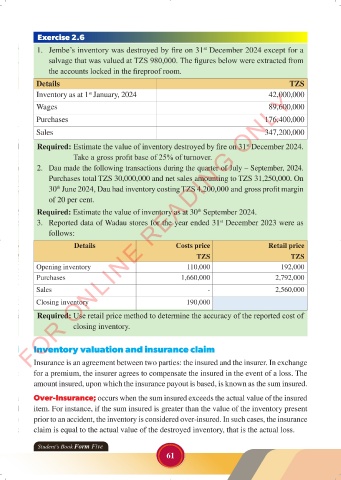

Exercise 2.6

1. Jembe’s inventory was destroyed by fire on 31 December 2024 except for a

st

salvage that was valued at TZS 980,000. The figures below were extracted from

the accounts locked in the fireproof room.

Details TZS

FOR ONLINE READING ONLY

Inventory as at 1 January, 2024 42,000,000

st

Wages 89,600,000

Purchases 176,400,000

LANGUAGE EDITING

Sales 347,200,000

LANGUAGE EDITING

Required: Estimate the value of inventory destroyed by fire on 31 December 2024.

st

Take a gross profit base of 25% of turnover.

2. Dau made the following transactions during the quarter of July – September, 2024.

Purchases total TZS 30,000,000 and net sales amounting to TZS 31,250,000. On

30 June 2024, Dau had inventory costing TZS 4,200,000 and gross profit margin

th

of 20 per cent.

Required: Estimate the value of inventory as at 30 September 2024.

th

3. Reported data of Wadau stores for the year ended 31 December 2023 were as

st

follows:

Details Costs price Retail price

TZS TZS

Opening inventory 110,000 192,000

Purchases 1,660,000 2,792,000

Sales - 2,560,000

Closing inventory 190,000

Required: Use retail price method to determine the accuracy of the reported cost of

closing inventory.

Inventory valuation and insurance claim

Insurance is an agreement between two parties: the insured and the insurer. In exchange

for a premium, the insurer agrees to compensate the insured in the event of a loss. The

amount insured, upon which the insurance payout is based, is known as the sum insured.

Over-Insurance; occurs when the sum insured exceeds the actual value of the insured

item. For instance, if the sum insured is greater than the value of the inventory present

prior to an accident, the inventory is considered over-insured. In such cases, the insurance

claim is equal to the actual value of the destroyed inventory, that is the actual loss.

Student’s Book Form Five

61

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 61 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 61