Page 72 - Accountancy_F5

P. 72

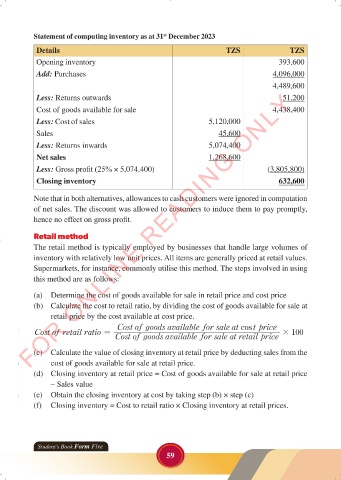

Statement of computing inventory as at 31 December 2023

st

Details TZS TZS

Opening inventory 393,600

Add: Purchases 4,096,000

4,489,600

FOR ONLINE READING ONLY

Less: Returns outwards 51,200

Cost of goods available for sale 4,438,400

LANGUAGE EDITING

Less: Cost of sales 5,120,000

Sales 45,600

LANGUAGE EDITING

Less: Returns inwards 5,074,400

Net sales 1,268,600

Less: Gross profit (25% × 5,074,400) (3,805,800)

Closing inventory 632,600

Note that in both alternatives, allowances to cash customers were ignored in computation

of net sales. The discount was allowed to customers to induce them to pay promptly,

hence no effect on gross profit.

Retail method

The retail method is typically employed by businesses that handle large volumes of

inventory with relatively low unit prices. All items are generally priced at retail values.

Supermarkets, for instance, commonly utilise this method. The steps involved in using

this method are as follows:

(a) Determine the cost of goods available for sale in retail price and cost price

(b) Calculate the cost to retail ratio, by dividing the cost of goods available for sale at

retail price by the cost available at cost price.

Cost of goods available for sale at cost price

Cost of retail ratio = # 100

Cost of goods available for sale at retail price

(c) Calculate the value of closing inventory at retail price by deducting sales from the

cost of goods available for sale at retail price.

(d) Closing inventory at retail price = Cost of goods available for sale at retail price

– Sales value

(e) Obtain the closing inventory at cost by taking step (b) × step (c)

(f) Closing inventory = Cost to retail ratio × Closing inventory at retail prices.

Student’s Book Form Five

59

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 59

ACCOUNTANCY_DUMMY_23 JUNE.indd 59 23/06/2024 17:35