Page 67 - Accountancy_F5

P. 67

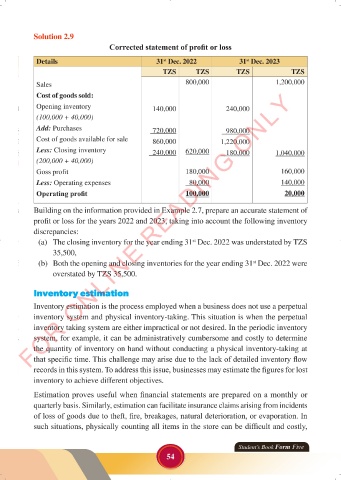

Solution 2.9

Corrected statement of profit or loss

Details 31 Dec. 2022 31 Dec. 2023

st

st

TZS TZS TZS TZS

Sales 800,000 1,200,000

FOR ONLINE READING ONLY

Cost of goods sold:

Opening inventory 140,000 240,000

(100,000 + 40,000)

Add: Purchases 720,000 980,000

LANGUAGE EDITING

Cost of goods available for sale 860,000 1,220,000

Less: Closing inventory 240,000 620,000 180,000 1,040,000

(200,000 + 40,000)

Goss profit 180,000 160,000

Less: Operating expenses 80,000 140,000

Operating profit 100,000 20,000

Building on the information provided in Example 2.7, prepare an accurate statement of

profit or loss for the years 2022 and 2023, taking into account the following inventory

discrepancies:

(a) The closing inventory for the year ending 31 Dec. 2022 was understated by TZS

st

35,500,

(b) Both the opening and closing inventories for the year ending 31 Dec. 2022 were

st

overstated by TZS 35,500.

Inventory estimation

Inventory estimation is the process employed when a business does not use a perpetual

inventory system and physical inventory-taking. This situation is when the perpetual

inventory taking system are either impractical or not desired. In the periodic inventory

system, for example, it can be administratively cumbersome and costly to determine

the quantity of inventory on hand without conducting a physical inventory-taking at

that specific time. This challenge may arise due to the lack of detailed inventory flow

records in this system. To address this issue, businesses may estimate the figures for lost

inventory to achieve different objectives.

Estimation proves useful when financial statements are prepared on a monthly or

quarterly basis. Similarly, estimation can facilitate insurance claims arising from incidents

of loss of goods due to theft, fire, breakages, natural deterioration, or evaporation. In

such situations, physically counting all items in the store can be difficult and costly,

Student’s Book Form Five

54

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 54

ACCOUNTANCY_DUMMY_23 JUNE.indd 54 23/06/2024 17:34