Page 65 - Accountancy_F5

P. 65

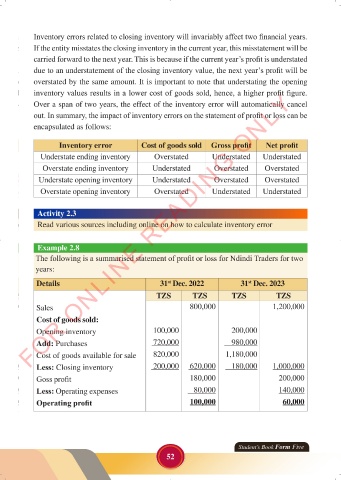

Inventory errors related to closing inventory will invariably affect two financial years.

If the entity misstates the closing inventory in the current year, this misstatement will be

carried forward to the next year. This is because if the current year’s profit is understated

due to an understatement of the closing inventory value, the next year’s profit will be

overstated by the same amount. It is important to note that understating the opening

FOR ONLINE READING ONLY

inventory values results in a lower cost of goods sold, hence, a higher profit figure.

Over a span of two years, the effect of the inventory error will automatically cancel

out. In summary, the impact of inventory errors on the statement of profit or loss can be

encapsulated as follows:r

LANGUAGE EDITING

Inventory error Cost of goods sold Gross profit Net profit

Understate ending inventory Overstated Understated Understated

Overstate ending inventory Understated Overstated Overstated

Understate opening inventory Understated Overstated Overstated

Overstate opening inventory Overstated Understated Understated

Activity 2.3

Read various sources including online on how to calculate inventory error

Example 2.8

The following is a summarised statement of profit or loss for Ndindi Traders for two

years:

Details 31 Dec. 2022 31 Dec. 2023

st

st

TZS TZS TZS TZS

Sales 800,000 1,200,000

Cost of goods sold:

Opening inventory 100,000 200,000

Add: Purchases 720,000 980,000

Cost of goods available for sale 820,000 1,180,000

Less: Closing inventory 200,000 620,000 180,000 1,000,000

Goss profit 180,000 200,000

Less: Operating expenses 80,000 140,000

Operating profit 100,000 60,000

Student’s Book Form Five

52

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 52 23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 52