Page 62 - Accountancy_F5

P. 62

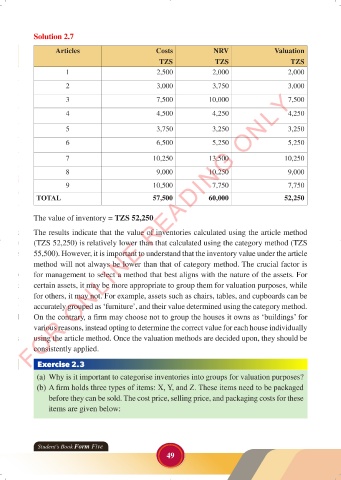

Solution 2.7

Articles Costs NRV Valuation

TZS TZS TZS

1 2,500 2,000 2,000

2 3,000 3,750 3,000

FOR ONLINE READING ONLY

3 7,500 10,000 7,500

4 4,500 4,250 4,250

5 3,750 3,250

LANGUAGE EDITING 3,250

LANGUAGE EDITING

6 6,500 5,250 5,250

7 10,250 13,500 10,250

8 9,000 10,250 9,000

9 10,500 7,750 7,750

TOTAL 57,500 60,000 52,250

The value of inventory = TZS 52,250

The results indicate that the value of inventories calculated using the article method

(TZS 52,250) is relatively lower than that calculated using the category method (TZS

55,500). However, it is important to understand that the inventory value under the article

method will not always be lower than that of category method. The crucial factor is

for management to select a method that best aligns with the nature of the assets. For

certain assets, it may be more appropriate to group them for valuation purposes, while

for others, it may not. For example, assets such as chairs, tables, and cupboards can be

accurately grouped as ‘furniture’, and their value determined using the category method.

On the contrary, a firm may choose not to group the houses it owns as ‘buildings’ for

various reasons, instead opting to determine the correct value for each house individually

using the article method. Once the valuation methods are decided upon, they should be

consistently applied.

Exercise 2.3

(a) Why is it important to categorise inventories into groups for valuation purposes?

(b) A firm holds three types of items: X, Y, and Z. These items need to be packaged

before they can be sold. The cost price, selling price, and packaging costs for these

items are given below:

Student’s Book Form Five

49

23/06/2024 17:34

ACCOUNTANCY_DUMMY_23 JUNE.indd 49

ACCOUNTANCY_DUMMY_23 JUNE.indd 49 23/06/2024 17:34