Page 114 - Book-keeping for Secondary Schools Student’s Book Form One

P. 114

Book-Keeping for Secondary Schools

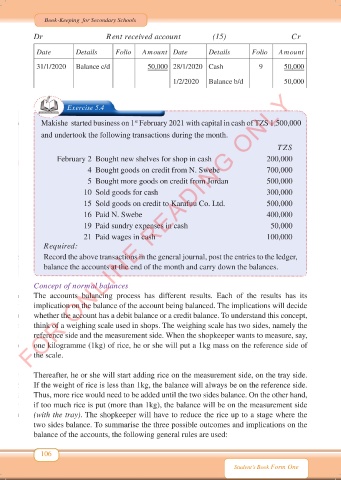

Dr Rent received account (15) Cr

Date Details Folio Amount Date Details Folio Amount

31/1/2020 Balance c/d 50,000 28/1/2020 Cash 9 50,000

1/2/2020 Balance b/d 50,000

FOR ONLINE READING ONLY

Exercise 5.4

Makishe started business on 1 February 2021 with capital in cash of TZS 1,500,000

st

and undertook the following transactions during the month.

TZS

February 2 Bought new shelves for shop in cash 200,000

4 Bought goods on credit from N. Swebe 700,000

5 Bought more goods on credit from Jordan 500,000

10 Sold goods for cash 300,000

15 Sold goods on credit to Karafuu Co. Ltd. 500,000

16 Paid N. Swebe 400,000

19 Paid sundry expenses in cash 50,000

21 Paid wages in cash 100,000

Required:

Record the above transactions in the general journal, post the entries to the ledger,

balance the accounts at the end of the month and carry down the balances.

Concept of normal balances

The accounts balancing process has different results. Each of the results has its

implication on the balance of the account being balanced. The implications will decide

whether the account has a debit balance or a credit balance. To understand this concept,

think of a weighing scale used in shops. The weighing scale has two sides, namely the

reference side and the measurement side. When the shopkeeper wants to measure, say,

one kilogramme (1kg) of rice, he or she will put a 1kg mass on the reference side of

the scale.

Thereafter, he or she will start adding rice on the measurement side, on the tray side.

If the weight of rice is less than 1kg, the balance will always be on the reference side.

Thus, more rice would need to be added until the two sides balance. On the other hand,

if too much rice is put (more than 1kg), the balance will be on the measurement side

(with the tray). The shopkeeper will have to reduce the rice up to a stage where the

two sides balance. To summarise the three possible outcomes and implications on the

balance of the accounts, the following general rules are used:

106

Student’s Book Form One

Book Keeping Form 1 New 2024 FINAL.indd 106 18/10/2024 10:14