Page 115 - Book-keeping for Secondary Schools Student’s Book Form One

P. 115

Ledgers

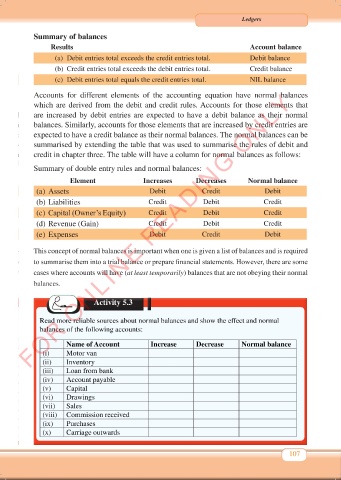

Summary of balances

Results Account balance

(a) Debit entries total exceeds the credit entries total. Debit balance

(b) Credit entries total exceeds the debit entries total. Credit balance

(c) Debit entries total equals the credit entries total. NIL balance

FOR ONLINE READING ONLY

Accounts for different elements of the accounting equation have normal balances

which are derived from the debit and credit rules. Accounts for those elements that

are increased by debit entries are expected to have a debit balance as their normal

balances. Similarly, accounts for those elements that are increased by credit entries are

expected to have a credit balance as their normal balances. The normal balances can be

summarised by extending the table that was used to summarise the rules of debit and

credit in chapter three. The table will have a column for normal balances as follows:

Summary of double entry rules and normal balances:

Element Increases Decreases Normal balance

(a) Assets Debit Credit Debit

(b) Liabilities Credit Debit Credit

(c) Capital (Owner’s Equity) Credit Debit Credit

(d) Revenue (Gain) Credit Debit Credit

(e) Expenses Debit Credit Debit

This concept of normal balances is important when one is given a list of balances and is required

to summarise them into a trial balance or prepare financial statements. However, there are some

cases where accounts will have (at least temporarily) balances that are not obeying their normal

balances.

Activity 5.3

Read more reliable sources about normal balances and show the effect and normal

balances of the following accounts:

Name of Account Increase Decrease Normal balance

(i) Motor van

(ii) Inventory

(iii) Loan from bank

(iv) Account payable

(v) Capital

(vi) Drawings

(vii) Sales

(viii) Commission received

(ix) Purchases

(x) Carriage outwards

107

Book Keeping Form 1 New 2024 FINAL.indd 107 18/10/2024 10:14