Page 35 - Book-keeping for Secondary Schools Student’s Book Form One

P. 35

Application of the double entry system

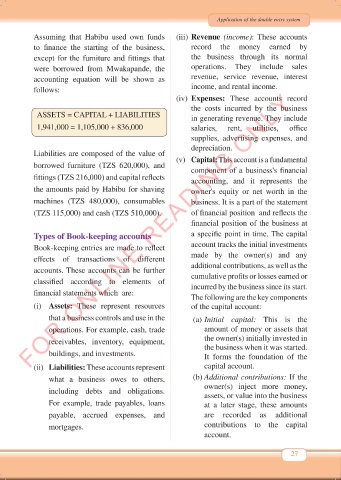

Assuming that Habibu used own funds (iii) Revenue (income): These accounts

to finance the starting of the business, record the money earned by

except for the furniture and fittings that the business through its normal

were borrowed from Mwakapande, the operations. They include sales

accounting equation will be shown as revenue, service revenue, interest

follows: income, and rental income.

FOR ONLINE READING ONLY

(iv) Expenses: These accounts record

the costs incurred by the business

ASSETS = CAPITAL + LIABILITIES in generating revenue. They include

1,941,000 = 1,105,000 + 836,000 salaries, rent, utilities, office

supplies, advertising expenses, and

depreciation.

Liabilities are composed of the value of (v) Capital: This account is a fundamental

borrowed furniture (TZS 620,000), and component of a business's financial

fittings (TZS 216,000) and capital reflects accounting, and it represents the

the amounts paid by Habibu for shaving owner's equity or net worth in the

machines (TZS 480,000), consumables business. It is a part of the statement

(TZS 115,000) and cash (TZS 510,000). of financial position and reflects the

financial position of the business at

Types of Book-keeping accounts a specific point in time. The capital

Book-keeping entries are made to reflect account tracks the initial investments

effects of transactions of different made by the owner(s) and any

accounts. These accounts can be further additional contributions, as well as the

classified according to elements of cumulative profits or losses earned or

incurred by the business since its start.

financial statements which are:

The following are the key components

(i) Assets: These represent resources of the capital account:

that a business controls and use in the (a) Initial capital: This is the

operations. For example, cash, trade amount of money or assets that

receivables, inventory, equipment, the owner(s) initially invested in

the business when it was started.

buildings, and investments. It forms the foundation of the

(ii) Liabilities: These accounts represent capital account.

what a business owes to others, (b) Additional contributions: If the

including debts and obligations. owner(s) inject more money,

assets, or value into the business

For example, trade payables, loans at a later stage, these amounts

payable, accrued expenses, and are recorded as additional

mortgages. contributions to the capital

account.

27

Book Keeping Form 1 New 2024 FINAL.indd 27 18/10/2024 10:14