Page 84 - Book-keeping for Secondary Schools Student’s Book Form One

P. 84

Book-Keeping for Secondary Schools

statements are from ledgers. Entries of different transactions are posted to the ledgers

from the books of prime entries. The posting is done to specific accounts in the ledgers.

Format of a ledger

A ledger contains specific records called accounts. An account is a record which shows

increases and decreases of a specific asset, liability, revenue, expense or capital item

FOR ONLINE READING ONLY

in the ledger. The ledger account has two sides. These are the left-hand side, which is

called the debit side (abbreviated as Dr.) and the right-hand side which is called the

credit side (abbreviated as Cr.). For the purpose of recording important details, each

ledger account must has a name or title. Additionally, each side of the ledger account

has the following columns:

(i) Date

This column is used to write the date, month, and year of the transaction.

(ii) Particulars

This column indicates the short description of the entry for the transaction recorded.

In the ledger account, this column indicates the name of the account to which the

corresponding entry has been made for the transaction (remember the principle of

double entry).

(iii) Folio

This column records pages of reference in books of accounts.

(iv) Amount

This column records the amount of money being transacted.

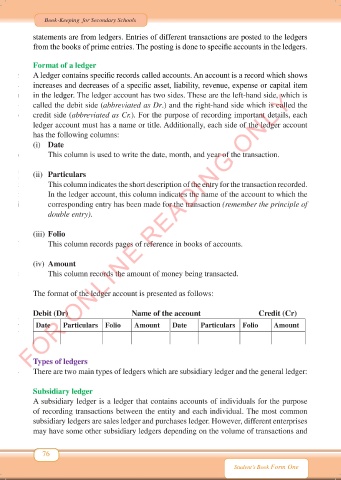

The format of the ledger account is presented as follows:

Debit (Dr) Name of the account Credit (Cr)

Date Particulars Folio Amount Date Particulars Folio Amount

Types of ledgers

There are two main types of ledgers which are subsidiary ledger and the general ledger:

Subsidiary ledger

A subsidiary ledger is a ledger that contains accounts of individuals for the purpose

of recording transactions between the entity and each individual. The most common

subsidiary ledgers are sales ledger and purchases ledger. However, different enterprises

may have some other subsidiary ledgers depending on the volume of transactions and

76

Student’s Book Form One

Book Keeping Form 1 New 2024 FINAL.indd 76 18/10/2024 10:14