Page 179 - Accountancy_F5

P. 179

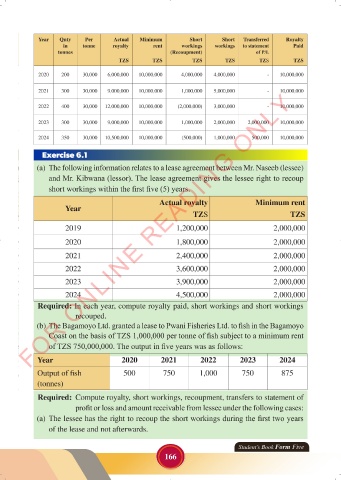

Year Qnty Per Actual Minimum Short Short Transferred Royalty

in tonne royalty rent workings workings to statement Paid

tonnes (Recoupment) of P/L

TZS TZS TZS TZS TZS TZS

2020 200 30,000 6,000,000 10,000,000 4,000,000 4,000,000 - 10,000,000

FOR ONLINE READING ONLY

2021 300 30,000 9,000,000 10,000,000 1,000,000 5,000,000 - 10,000,000

2022 400 30,000 12,000,000 10,000,000 (2,000,000) 3,000,000 - 10,000,000

2023 300 30,000 9,000,000 10,000,000 1,000,000 2,000,000 2,000,000 10,000,000

2024 350 30,000 10,500,000 10,000,000 (500,000) 1,000,000 500,000 10,000,000

LANGUAGE EDITING

Exercise 6.1

(a) The following information relates to a lease agreement between Mr. Naseeb (lessee)

and Mr. Kibwana (lessor). The lease agreement gives the lessee right to recoup

short workings within the first five (5) years.

Actual royalty Minimum rent

Year

TZS TZS

2019 1,200,000 2,000,000

2020 1,800,000 2,000,000

2021 2,400,000 2,000,000

2022 3,600,000 2,000,000

2023 3,900,000 2,000,000

2024 4,500,000 2,000,000

Required: In each year, compute royalty paid, short workings and short workings

recouped.

(b) The Bagamoyo Ltd. granted a lease to Pwani Fisheries Ltd. to fish in the Bagamoyo

Coast on the basis of TZS 1,000,000 per tonne of fish subject to a minimum rent

of TZS 750,000,000. The output in five years was as follows:

Year 2020 2021 2022 2023 2024

Output of fish 500 750 1,000 750 875

(tonnes)

Required: Compute royalty, short workings, recoupment, transfers to statement of

profit or loss and amount receivable from lessee under the following cases:

(a) The lessee has the right to recoup the short workings during the first two years

of the lease and not afterwards.

Student’s Book Form Five

166

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 166

ACCOUNTANCY_DUMMY_23 JUNE.indd 166 23/06/2024 17:35