Page 102 - Accountancy_F5

P. 102

Preparation of payroll accounts

Employers maintain records with information of each employee salary including hours

worked, the rate of pay, total overtime, entitlement and additions to salary, reductions

from salary and employee’s net salary pay. Payroll records refer to documents kept by

entities for recording payroll transactions or information. Basically, the two major payroll

FOR ONLINE READING ONLY

records are individual earning statement (salary slip) and payroll summaries.

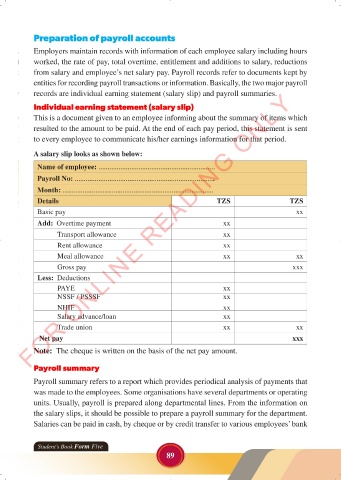

Individual earning statement (salary slip)

This is a document given to an employee informing about the summary of items which

resulted to the amount to be paid. At the end of each pay period, this statement

LANGUAGE EDITINGis sent

to every employee to communicate his/her earnings information for that period.

LANGUAGE EDITING

A salary slip looks as shown below:

Name of employee: ................................................................

Payroll No: .............................................................................

Month: ...................................................................................

Details TZS TZS

Basic pay xx

Add: Overtime payment xx

Transport allowance xx

Rent allowance xx

Meal allowance xx xx

Gross pay xxx

Less: Deductions

PAYE xx

NSSF / PSSSF xx

NHIF xx

Salary advance/loan xx

Trade union xx xx

Net pay xxx

Note: The cheque is written on the basis of the net pay amount.

Payroll summary

Payroll summary refers to a report which provides periodical analysis of payments that

was made to the employees. Some organisations have several departments or operating

units. Usually, payroll is prepared along departmental lines. From the information on

the salary slips, it should be possible to prepare a payroll summary for the department.

Salaries can be paid in cash, by cheque or by credit transfer to various employees’ bank

Student’s Book Form Five

89

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 89

ACCOUNTANCY_DUMMY_23 JUNE.indd 89 23/06/2024 17:35