Page 104 - Accountancy_F5

P. 104

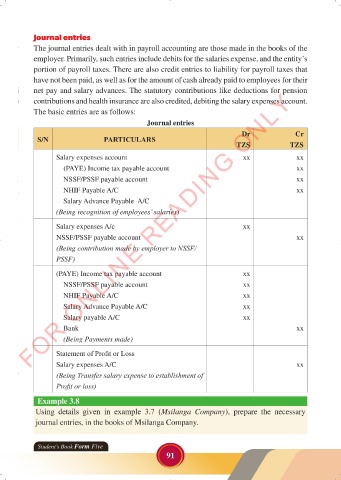

Journal entries

The journal entries dealt with in payroll accounting are those made in the books of the

employer. Primarily, such entries include debits for the salaries expense, and the entity’s

portion of payroll taxes. There are also credit entries to liability for payroll taxes that

have not been paid, as well as for the amount of cash already paid to employees for their

net pay and salary advances. The statutory contributions like deductions for pension

FOR ONLINE READING ONLY

contributions and health insurance are also credited, debiting the salary expenses account.

The basic entries are as follows:

LANGUAGE EDITING

Journal entries

Dr Cr

S/N PARTICULARS

LANGUAGE EDITING

TZS TZS

Salary expenses account xx xx

(PAYE) Income tax payable account xx

NSSF/PSSF payable account xx

NHIF Payable A/C xx

Salary Advance Payable A/C

(Being recognition of employees’ salaries)

Salary expenses A/c xx

NSSF/PSSF payable account xx

(Being contribution made by employer to NSSF/

PSSF)

(PAYE) Income tax payable account xx

NSSF/PSSF payable account xx

NHIF Payable A/C xx

Salary Advance Payable A/C xx

Salary payable A/C xx

Bank xx

(Being Payments made)

Statement of Profit or Loss

Salary expenses A/C xx

(Being Transfer salary expense to establishment of

Profit or loss)

Example 3.8

Using details given in example 3.7 (Msilanga Company), prepare the necessary

journal entries, in the books of Msilanga Company.

Student’s Book Form Five

91

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 91 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 91