Page 105 - Accountancy_F5

P. 105

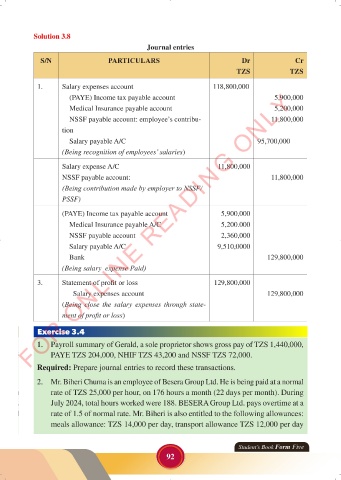

Solution 3.8

Journal entries

S/N PARTICULARS Dr Cr

TZS TZS

1. Salary expenses account 118,800,000

FOR ONLINE READING ONLY

(PAYE) Income tax payable account 5,900,000

Medical Insurance payable account 5,200,000

NSSF payable account: employee’s contribu- 11,800,000

tion

LANGUAGE EDITING

Salary payable A/C 95,700,000

(Being recognition of employees’ salaries)

Salary expense A/C 11,800,000

NSSF payable account: 11,800,000

(Being contribution made by employer to NSSF/

PSSF)

(PAYE) Income tax payable account 5,900,000

Medical Insurance payable A/C 5,200.000

NSSF payable account 2,360,000

Salary payable A/C 9,510,0000

Bank 129,800,000

(Being salary expense Paid)

3. Statement of profit or loss 129,800,000

Salary expenses account 129,800,000

(Being close the salary expenses through state-

ment of profit or loss)

Exercise 3.4

1. Payroll summary of Gerald, a sole proprietor shows gross pay of TZS 1,440,000,

PAYE TZS 204,000, NHIF TZS 43,200 and NSSF TZS 72,000.

Required: Prepare journal entries to record these transactions.

2. Mr. Biheri Chuma is an employee of Besera Group Ltd. He is being paid at a normal

rate of TZS 25,000 per hour, on 176 hours a month (22 days per month). During

July 2024, total hours worked were 188. BESERA Group Ltd. pays overtime at a

rate of 1.5 of normal rate. Mr. Biheri is also entitled to the following allowances:

meals allowance: TZS 14,000 per day, transport allowance TZS 12,000 per day

Student’s Book Form Five

92

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 92

ACCOUNTANCY_DUMMY_23 JUNE.indd 92 23/06/2024 17:35