Page 191 - Accountancy_F5

P. 191

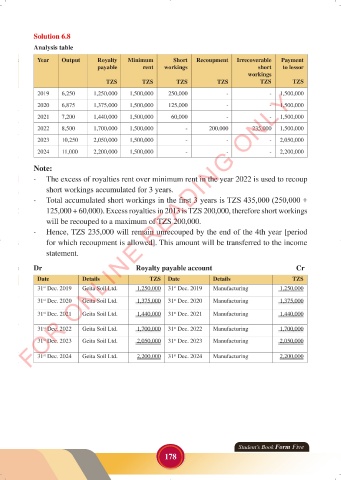

Solution 6.8

Analysis table

Year Output Royalty Minimum Short Recoupment Irrecoverable Payment

payable rent workings short to lessor

workings

TZS TZS TZS TZS TZS TZS

FOR ONLINE READING ONLY

2019 6,250 1,250,000 1,500,000 250,000 - - 1,500,000

2020 6,875 1,375,000 1,500,000 125,000 - - 1,500,000

2021 7,200 1,440,000 1,500,000 60,000 - - 1,500,000

2022 8,500 1,700,000 1,500,000 - 200,000 235,000 1,500,000

LANGUAGE EDITING

2023 10,250 2,050,000 1,500,000 - - - 2,050,000

2024 11,000 2,200,000 1,500,000 - - - 2,200,000

Note:

- The excess of royalties rent over minimum rent in the year 2022 is used to recoup

short workings accumulated for 3 years.

- Total accumulated short workings in the first 3 years is TZS 435,000 (250,000 +

125,000 + 60,000). Excess royalties in 2013 is TZS 200,000, therefore short workings

will be recouped to a maximum of TZS 200,000.

- Hence, TZS 235,000 will remain unrecouped by the end of the 4th year [period

for which recoupment is allowed]. This amount will be transferred to the income

statement.

Dr Royalty payable account Cr

Date Details TZS Date Details TZS

31 Dec. 2019 Geita Soil Ltd. 1,250,000 31 Dec. 2019 Manufacturing 1,250,000

st

st

st

31 Dec. 2020 Geita Soil Ltd. 1,375,000 31 Dec. 2020 Manufacturing 1,375,000

st

31 Dec. 2021 Geita Soil Ltd. 1,440,000 31 Dec. 2021 Manufacturing 1,440,000

st

st

31 Dec. 2022 Geita Soil Ltd. 1,700,000 31 Dec. 2022 Manufacturing 1,700,000

st

st

31 Dec. 2023 Geita Soil Ltd. 2,050,000 31 Dec. 2023 Manufacturing 2,050,000

st

st

31 Dec. 2024 Geita Soil Ltd. 2,200,000 31 Dec. 2024 Manufacturing 2,200,000

st

st

Student’s Book Form Five

178

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 178 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 178