Page 195 - Accountancy_F5

P. 195

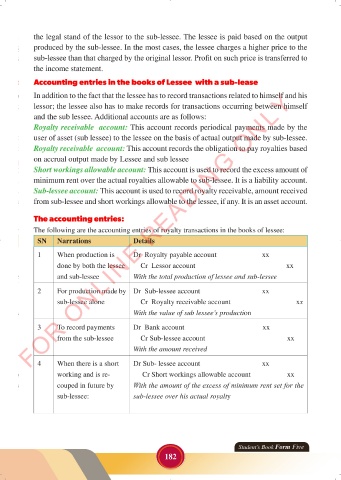

the legal stand of the lessor to the sub-lessee. The lessee is paid based on the output

produced by the sub-lessee. In the most cases, the lessee charges a higher price to the

sub-lessee than that charged by the original lessor. Profit on such price is transferred to

the income statement.

Accounting entries in the books of Lessee with a sub-lease

FOR ONLINE READING ONLY

In addition to the fact that the lessee has to record transactions related to himself and his

lessor; the lessee also has to make records for transactions occurring between himself

and the sub lessee. Additional accounts are as follows:

Royalty receivable account: This account records periodical payments made by the

user of asset (sub lessee) to the lessee on the basis of actual output made by sub-lessee.

LANGUAGE EDITING

Royalty receivable account: This account records the obligation to pay royalties based

on accrual output made by Lessee and sub lessee

Short workings allowable account: This account is used to record the excess amount of

minimum rent over the actual royalties allowable to sub-lessee. It is a liability account.

Sub-lessee account: This account is used to record royalty receivable, amount received

from sub-lessee and short workings allowable to the lessee, if any. It is an asset account.

The accounting entries:

The following are the accounting entries of royalty transactions in the books of lessee:

SN Narrations Details

1 When production is Dr Royalty payable account xx

done by both the lessee Cr Lessor account xx

and sub-lessee With the total production of lessee and sub-lessee

2 For production made by Dr Sub-lessee account xx

sub-lessee alone Cr Royalty receivable account xx

With the value of sub lessee’s production

3 To record payments Dr Bank account xx

from the sub-lessee Cr Sub-lessee account xx

With the amount received

4 When there is a short Dr Sub- lessee account xx

working and is re- Cr Short workings allowable account xx

couped in future by With the amount of the excess of minimum rent set for the

sub-lessee: sub-lessee over his actual royalty

Student’s Book Form Five

182

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 182 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 182