Page 200 - Accountancy_F5

P. 200

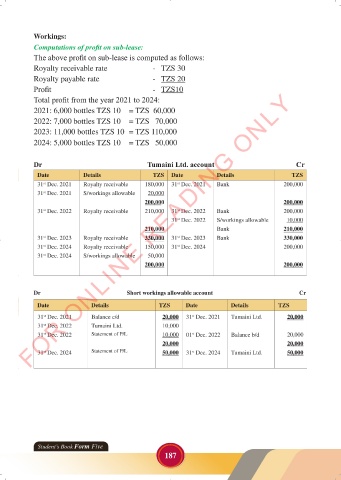

Workings:

Computations of profit on sub-lease:

The above profit on sub-lease is computed as follows:

Royalty receivable rate - TZS 30

Royalty payable rate - TZS 20

Profit - TZS10

FOR ONLINE READING ONLY

Total profit from the year 2021 to 2024:

2021: 6,000 bottles TZS 10 = TZS 60,000

LANGUAGE EDITING

2022: 7,000 bottles TZS 10 = TZS 70,000

2023: 11,000 bottles TZS 10 = TZS 110,000

LANGUAGE EDITING

2024: 5,000 bottles TZS 10 = TZS 50,000

Dr Tumaini Ltd. account Cr

Date Details TZS Date Details TZS

31 Dec. 2021 Royalty receivable 180,000 31 Dec. 2021 Bank 200,000

st

st

31 Dec. 2021 S/workings allowable 20,000

st

200,000 200,000

31 Dec. 2022 Royalty receivable 210,000 31 Dec. 2022 Bank 200,000

st

st

31 Dec. 2022 S/workings allowable 10,000

st

210,000 Bank 210,000

31 Dec. 2023 Royalty receivable 330,000 31 Dec. 2023 Bank 330,000

st

st

31 Dec. 2024 Royalty receivable 150,000 31 Dec. 2024 200,000

st

st

31 Dec. 2024 S/workings allowable 50,000

st

200,000 200,000

Dr Short workings allowable account Cr

Date Details TZS Date Details TZS

31 Dec. 2021 Balance c/d 20,000 31 Dec. 2021 Tumaini Ltd. 20,000

st

st

31 Dec. 2022 Tumaini Ltd. 10,000

st

31 Dec. 2022 Statement of P/L 10,000 01 Dec. 2022 Balance b/d 20,000

st

st

20,000 20,000

31 Dec. 2024 Statement of P/L 50,000 31 Dec. 2024 Tumaini Ltd. 50,000

st

st

Student’s Book Form Five

187

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 187

ACCOUNTANCY_DUMMY_23 JUNE.indd 187 23/06/2024 17:35