Page 201 - Accountancy_F5

P. 201

Exercise 6.3

1. Deka Ltd. acquired rights from Nassa Ltd. to manufacture and sell a certain brand

of perfume on the following terms:

(a) Royalty shall be paid on number of bottles manufactured at TZS200 per bottle.

(b) The minimum royalty in any one year shall be TZS500,000.

FOR ONLINE READING ONLY

(c) Short workings will be recouped within the first three years of the contract.

(d) The agreement to become effective on 1 July 2018; and

st

(e) All settlements were made on 31 December, each year.

st

On 1 January 2020, Deka Ltd. granted right to Mwinula Ltd. to manufacture

st

and sell the same perfumes on the following terms:

LANGUAGE EDITING

(i) Royalty shall be paid on number of bottles manufactured at TZS 300 per bottle/

per unit;

(ii) The minimum royalty in any one year shall be TZS200,000; and

(iii) Short workings recouped only in the year of agreement following the year of

short workings.

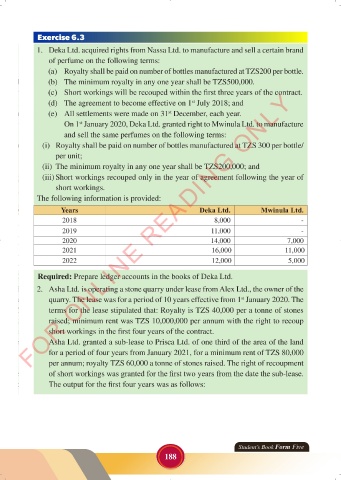

The following information is provided:

Years Deka Ltd. Mwinula Ltd.

2018 8,000 -

2019 11,000 -

2020 14,000 7,000

2021 16,000 11,000

2022 12,000 5,000

Required: Prepare ledger accounts in the books of Deka Ltd.

2. Asha Ltd. is operating a stone quarry under lease from Alex Ltd., the owner of the

quarry. The lease was for a period of 10 years effective from 1 January 2020. The

st

terms for the lease stipulated that: Royalty is TZS 40,000 per a tonne of stones

raised; minimum rent was TZS 10,000,000 per annum with the right to recoup

short workings in the first four years of the contract.

Asha Ltd. granted a sub-lease to Prisca Ltd. of one third of the area of the land

for a period of four years from January 2021, for a minimum rent of TZS 80,000

per annum; royalty TZS 60,000 a tonne of stones raised. The right of recoupment

of short workings was granted for the first two years from the date the sub-lease.

The output for the first four years was as follows:

Student’s Book Form Five

188

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 188 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 188