Page 196 - Accountancy_F5

P. 196

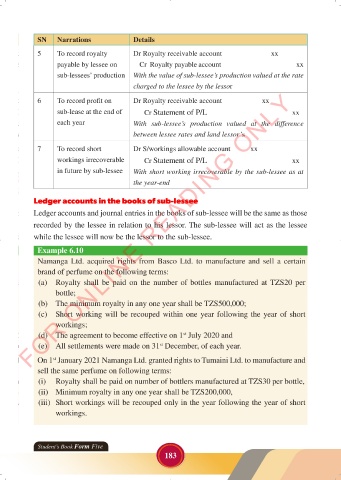

SN Narrations Details

5 To record royalty Dr Royalty receivable account xx

payable by lessee on Cr Royalty payable account xx

sub-lessees’ production With the value of sub-lessee’s production valued at the rate

charged to the lessee by the lessor

FOR ONLINE READING ONLY

6 To record profit on Dr Royalty receivable account xx

sub-lease at the end of Cr Statement of P/L xx

LANGUAGE EDITING

each year With sub-lessee’s production valued at the difference

between lessee rates and land lessor’s

LANGUAGE EDITING

7 To record short Dr S/workings allowable account xx

workings irrecoverable Cr Statement of P/L xx

in future by sub-lessee With short working irrecoverable by the sub-lessee as at

the year-end

Ledger accounts in the books of sub-lessee

Ledger accounts and journal entries in the books of sub-lessee will be the same as those

recorded by the lessee in relation to his lessor. The sub-lessee will act as the lessee

while the lessee will now be the lessor to the sub-lessee.

Example 6.10

Namanga Ltd. acquired rights from Basco Ltd. to manufacture and sell a certain

brand of perfume on the following terms:

(a) Royalty shall be paid on the number of bottles manufactured at TZS20 per

bottle;

(b) The minimum royalty in any one year shall be TZS500,000;

(c) Short working will be recouped within one year following the year of short

workings;

(d) The agreement to become effective on 1 July 2020 and

st

(e) All settlements were made on 31 December, of each year.

st

On 1 January 2021 Namanga Ltd. granted rights to Tumaini Ltd. to manufacture and

st

sell the same perfume on following terms:

(i) Royalty shall be paid on number of bottlers manufactured at TZS30 per bottle,

(ii) Minimum royalty in any one year shall be TZS200,000,

(iii) Short workings will be recouped only in the year following the year of short

workings.

Student’s Book Form Five

183

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 183 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 183