Page 242 - Accountancy_F5

P. 242

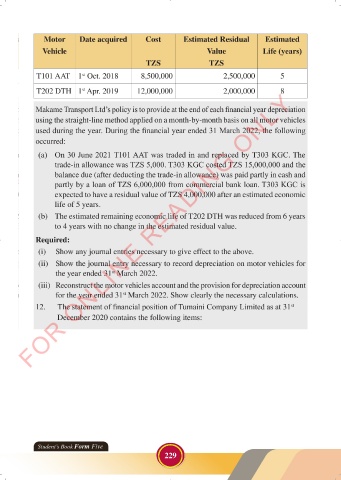

Motor Date acquired Cost Estimated Residual Estimated

Vehicle Value Life (years)

TZS TZS

T101 AAT 1 Oct. 2018 8,500,000 2,500,000 5

st

T202 DTH 1 Apr. 2019 12,000,000 2,000,000 8

FOR ONLINE READING ONLY

st

Makame Transport Ltd’s policy is to provide at the end of each financial year depreciation

using the straight-line method applied on a month-by-month basis on all motor vehicles

LANGUAGE EDITING

used during the year. During the financial year ended 31 March 2022, the following

LANGUAGE EDITING

occurred:

(a) On 30 June 2021 T101 AAT was traded in and replaced by T303 KGC. The

trade-in allowance was TZS 5,000. T303 KGC costed TZS 15,000,000 and the

balance due (after deducting the trade-in allowance) was paid partly in cash and

partly by a loan of TZS 6,000,000 from commercial bank loan. T303 KGC is

expected to have a residual value of TZS 4,000,000 after an estimated economic

life of 5 years.

(b) The estimated remaining economic life of T202 DTH was reduced from 6 years

to 4 years with no change in the estimated residual value.

Required:

(i) Show any journal entries necessary to give effect to the above.

(ii) Show the journal entry necessary to record depreciation on motor vehicles for

the year ended 31 March 2022.

st

(iii) Reconstruct the motor vehicles account and the provision for depreciation account

for the year ended 31 March 2022. Show clearly the necessary calculations.

st

12. The statement of financial position of Tumaini Company Limited as at 31 st

December 2020 contains the following items:

Student’s Book Form Five

229

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 229

ACCOUNTANCY_DUMMY_23 JUNE.indd 229 23/06/2024 17:36