Page 237 - Accountancy_F5

P. 237

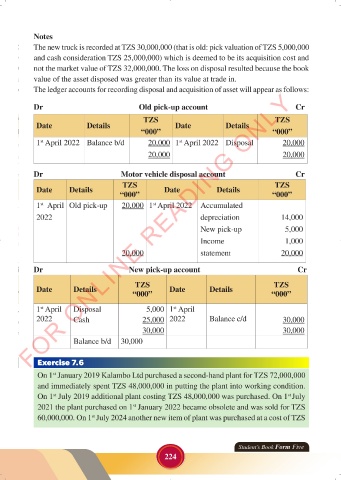

Notes

The new truck is recorded at TZS 30,000,000 (that is old: pick valuation of TZS 5,000,000

and cash consideration TZS 25,000,000) which is deemed to be its acquisition cost and

not the market value of TZS 32,000,000. The loss on disposal resulted because the book

value of the asset disposed was greater than its value at trade in.

The ledger accounts for recording disposal and acquisition of asset will appear as follows:

FOR ONLINE READING ONLY

Dr Old pick-up account Cr

TZS TZS

Date Details Date Details

“000” “000”

LANGUAGE EDITING

1 April 2022 Balance b/d 20,000 1 April 2022 Disposal 20,000

st

st

20,000 20,000

Dr Motor vehicle disposal account Cr

TZS TZS

Date Details Date Details

“000” “000”

1 April Old pick-up 20,000 1 April 2022 Accumulated

st

st

2022 depreciation 14,000

New pick-up 5,000

Income 1,000

20,000 statement 20,000

Dr New pick-up account Cr

TZS TZS

Date Details Date Details

“000” “000”

1 April Disposal 5,000 1 April

st

st

2022 Cash 25,000 2022 Balance c/d 30,000

30,000 30,000

Balance b/d 30,000

Exercise 7.6

On 1 January 2019 Kalambo Ltd purchased a second-hand plant for TZS 72,000,000

st

and immediately spent TZS 48,000,000 in putting the plant into working condition.

On 1 July 2019 additional plant costing TZS 48,000,000 was purchased. On 1 July

st

st

2021 the plant purchased on 1 January 2022 became obsolete and was sold for TZS

st

60,000,000. On 1 July 2024 another new item of plant was purchased at a cost of TZS

st

Student’s Book Form Five

224

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 224 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 224