Page 233 - Accountancy_F5

P. 233

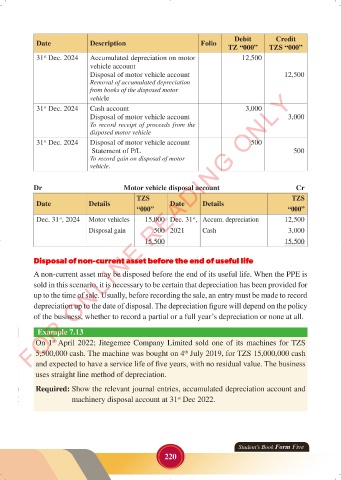

Date Description Folio Debit Credit

TZ “000” TZS “000”

31 Dec. 2024 Accumulated depreciation on motor 12,500

st

vehicle account

Disposal of motor vehicle account 12,500

Removal of accumulated depreciation

FOR ONLINE READING ONLY

from books of the disposed motor

vehicle

31 Dec. 2024 Cash account 3,000

st

Disposal of motor vehicle account 3,000

To record receipt of proceeds from the

disposed motor vehicle

LANGUAGE EDITING

31 Dec. 2024 Disposal of motor vehicle account 500

st

Statement of P/L 500

To record gain on disposal of motor

vehicle.

Dr Motor vehicle disposal account Cr

TZS TZS

Date Details Date Details

“000” “000”

Dec. 31 , 2024 Motor vehicles 15,000 Dec. 31 , Accum. depreciation 12,500

st

st

Disposal gain 500 2021 Cash 3,000

15,500 15,500

Disposal of non-current asset before the end of useful life

A non-current asset may be disposed before the end of its useful life. When the PPE is

sold in this scenario, it is necessary to be certain that depreciation has been provided for

up to the time of sale. Usually, before recording the sale, an entry must be made to record

depreciation up to the date of disposal. The depreciation figure will depend on the policy

of the business, whether to record a partial or a full year’s depreciation or none at all.

Example 7.13

On 1 April 2022; Jitegemee Company Limited sold one of its machines for TZS

st

5,500,000 cash. The machine was bought on 4 July 2019, for TZS 15,000,000 cash

th

and expected to have a service life of five years, with no residual value. The business

uses straight line method of depreciation.

Required: Show the relevant journal entries, accumulated depreciation account and

machinery disposal account at 31 Dec 2022.

st

Student’s Book Form Five

220

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 220

ACCOUNTANCY_DUMMY_23 JUNE.indd 220 23/06/2024 17:35