Page 236 - Accountancy_F5

P. 236

Activity 7.3

Consider two separate buildings in a school whereby one is used for classrooms and

the other as administration block, then respond on the following questions:

(i) If the two buildings were constructed at the same time and have the same quality,

will they have the same useful life? Explain with reasons.

(ii) With reasons, explain which of the depreciation methods covered in this chapter

FOR ONLINE READING ONLY

is appropriate to use in charging depreciation in each of the two buildings.

(iii) Explain possible way(s) for disposing the building once they reach the end of

their useful life.

LANGUAGE EDITING

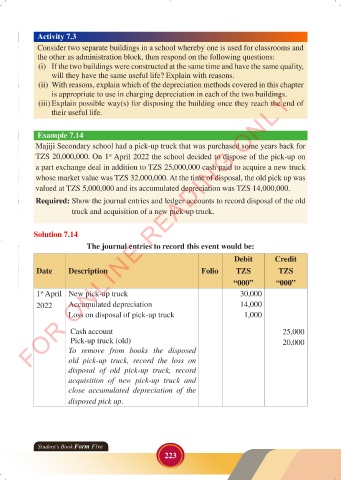

Example 7.14

LANGUAGE EDITING

Majiji Secondary school had a pick-up truck that was purchased some years back for

TZS 20,000,000. On 1 April 2022 the school decided to dispose of the pick-up on

st

a part exchange deal in addition to TZS 25,000,000 cash paid to acquire a new truck

whose market value was TZS 32,000,000. At the time of disposal, the old pick up was

valued at TZS 5,000,000 and its accumulated depreciation was TZS 14,000,000.

Required: Show the journal entries and ledger accounts to record disposal of the old

truck and acquisition of a new pick-up truck.

Solution 7.14

The journal entries to record this event would be:

Debit Credit

Date Description Folio TZS TZS

“000” “000”

1 April New pick-up truck 30,000

st

2022 Accumulated depreciation 14,000

Loss on disposal of pick-up truck 1,000

Cash account 25,000

Pick-up truck (old) 20,000

To remove from books the disposed

old pick-up truck, record the loss on

disposal of old pick-up truck, record

acquisition of new pick-up truck and

close accumulated depreciation of the

disposed pick up.

Student’s Book Form Five

223

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 223 23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 223