Page 232 - Accountancy_F5

P. 232

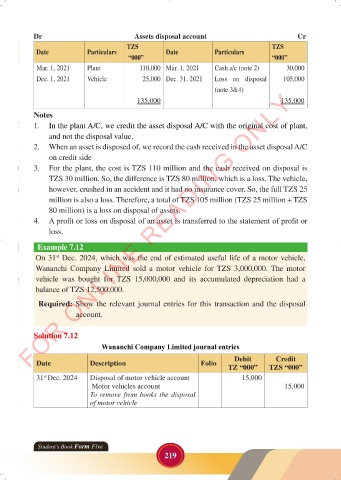

Dr Assets disposal account Cr

TZS TZS

Date Particulars Date Particulars

“000” “000”

Mar. 1, 2021 Plant 110,000 Mar. 1, 2021 Cash a/c (note 2) 30,000

Dec. 1, 2021 Vehicle 25,000 Dec. 31, 2021 Loss on disposal 105,000

(note 3&4)

FOR ONLINE READING ONLY

135,000 135,000

Notes

LANGUAGE EDITING

1. In the plant A/C, we credit the asset disposal A/C with the original cost of plant,

and not the disposal value.

LANGUAGE EDITING

2. When an asset is disposed of, we record the cash received in the asset disposal A/C

on credit side

3. For the plant, the cost is TZS 110 million and the cash received on disposal is

TZS 30 million. So, the difference is TZS 80 million, which is a loss. The vehicle,

however, crushed in an accident and it had no insurance cover. So, the full TZS 25

million is also a loss. Therefore, a total of TZS 105 million (TZS 25 million + TZS

80 million) is a loss on disposal of assets.

4. A profit or loss on disposal of an asset is transferred to the statement of profit or

loss.

Example 7.12

On 31 Dec. 2024, which was the end of estimated useful life of a motor vehicle,

st

Wananchi Company Limited sold a motor vehicle for TZS 3,000,000. The motor

vehicle was bought for TZS 15,000,000 and its accumulated depreciation had a

balance of TZS 12,500,000.

Required: Show the relevant journal entries for this transaction and the disposal

account.

Solution 7.12

Wananchi Company Limited journal entries

Debit Credit

Date Description Folio TZ “000” TZS “000”

31 Dec. 2024 Disposal of motor vehicle account 15,000

st

Motor vehicles account 15,000

To remove from books the disposal

of motor vehicle

Student’s Book Form Five

219

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 219

ACCOUNTANCY_DUMMY_23 JUNE.indd 219 23/06/2024 17:35