Page 231 - Accountancy_F5

P. 231

Disposal of non-current asset at the end of useful life

Usually, non-current assets are disposed at the end of its useful life. At that point, the

carrying value of an asset is its salvage value. Therefore, when the proceeds from

the disposal are equal to the net book value, then there is neither a gain nor a loss on

disposal. Meanwhile, if proceeds from the sale exceed the net book value, there is a gain

FOR ONLINE READING ONLY

on disposal and its vice versa is a loss.

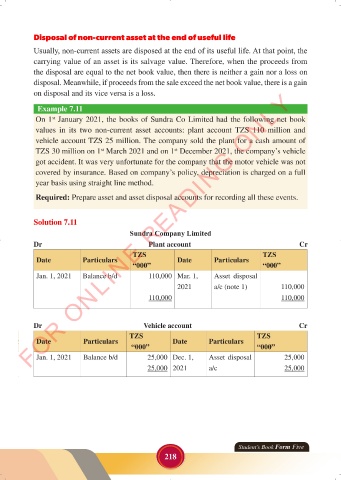

Example 7.11

On 1 January 2021, the books of Sundra Co Limited had the following net book

st

values in its two non-current asset accounts: plant account TZS 110 million and

LANGUAGE EDITING

vehicle account TZS 25 million. The company sold the plant for a cash amount of

TZS 30 million on 1 March 2021 and on 1 December 2021, the company’s vehicle

st

st

got accident. It was very unfortunate for the company that the motor vehicle was not

covered by insurance. Based on company’s policy, depreciation is charged on a full

year basis using straight line method.

Required: Prepare asset and asset disposal accounts for recording all these events.

Solution 7.11

Sundra Company Limited

Dr Plant account Cr

TZS TZS

Date Particulars Date Particulars

“000” “000”

Jan. 1, 2021 Balance b/d 110,000 Mar. 1, Asset disposal

2021 a/c (note 1) 110,000

110,000 110,000

Dr Vehicle account Cr

TZS TZS

Date Particulars Date Particulars

“000” “000”

Jan. 1, 2021 Balance b/d 25,000 Dec. 1, Asset disposal 25,000

25,000 2021 a/c 25,000

Student’s Book Form Five

218

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 218 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 218