Page 228 - Accountancy_F5

P. 228

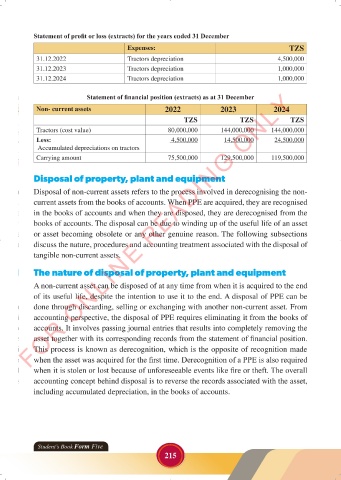

Statement of profit or loss (extracts) for the years ended 31 December

Expenses: TZS

31.12.2022 Tractors depreciation 4,500,000

31.12.2023 Tractors depreciation 1,000,000

31.12.2024 Tractors depreciation 1,000,000

FOR ONLINE READING ONLY

Statement of financial position (extracts) as at 31 December

Non- current assets 2022 2023 2024

TZS TZS TZS

LANGUAGE EDITING

Tractors (cost value) 80,000,000 144,000,000 144,000,000

LANGUAGE EDITING

Less: 4,500,000 14,500,000 24,500,000

Accumulated depreciations on tractors

Carrying amount 75,500,000 129,500,000 119,500,000

Disposal of property, plant and equipment

Disposal of non-current assets refers to the process involved in derecognising the non-

current assets from the books of accounts. When PPE are acquired, they are recognised

in the books of accounts and when they are disposed, they are derecognised from the

books of accounts. The disposal can be due to winding up of the useful life of an asset

or asset becoming obsolete or any other genuine reason. The following subsections

discuss the nature, procedures and accounting treatment associated with the disposal of

tangible non-current assets.

The nature of disposal of property, plant and equipment

A non-current asset can be disposed of at any time from when it is acquired to the end

of its useful life, despite the intention to use it to the end. A disposal of PPE can be

done through discarding, selling or exchanging with another non-current asset. From

accounting perspective, the disposal of PPE requires eliminating it from the books of

accounts. It involves passing journal entries that results into completely removing the

asset together with its corresponding records from the statement of financial position.

This process is known as derecognition, which is the opposite of recognition made

when the asset was acquired for the first time. Derecognition of a PPE is also required

when it is stolen or lost because of unforeseeable events like fire or theft. The overall

accounting concept behind disposal is to reverse the records associated with the asset,

including accumulated depreciation, in the books of accounts.

Student’s Book Form Five

215

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 215 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 215