Page 239 - Accountancy_F5

P. 239

loss on disposal. These entries are subsequently transferred to the income statement,

along with accumulated depreciation recorded in the statement of financial position,

ensuring accurate representation of the financial impact of asset disposals on financial

statements. Through thorough coverage of these topics, the chapter equips readers

with the knowledge and skills necessary to effectively manage depreciation and non-

current asset disposals, facilitating accurate financial reporting and decision-making

FOR ONLINE READING ONLY

processes.

Revision exercises

1. Describe the characteristics of an asset to be classified as non-current assets.

2. Differentiate tangible non-current assets from intangible non-current assets.

3. Using the matching concept and accruals as well as prudence concept, examine

the rationale for charging depreciation for tangible non-current assets.

4. A photographer owns a property, plant, and equipment worth TZS 10,000,000/=

and she estimates to use the equipment for five years with zero residual value.

Required: Compute the depreciation expenses for each of the five years.

5. SAHARA Company Limited purchased a machine for TZS 650,000 on 1st January,

2019. It had an estimated salvage value of TZS 100,000 and an estimated useful

life of five years. The company depreciates machinery on a straight-line basis.

Required: LANGUAGE EDITING

(a) How much will be the annual depreciation charge?

(b If the machine is sold at the end of its third year of use at TZS 280,000, what

will be the amount of profit or loss on the sale of this asset?

(c) Show the ledger accounts for machinery, provision for depreciation and

machinery disposal for the years 2019, 2020 and 2021.

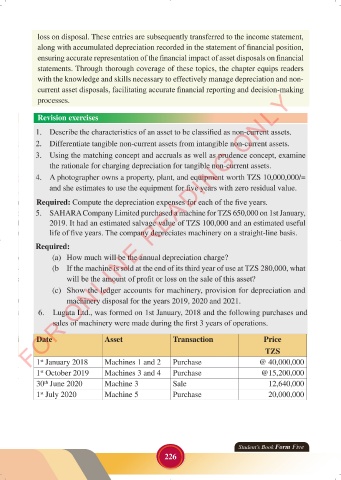

6. Lugata Ltd., was formed on 1st January, 2018 and the following purchases and

sales of machinery were made during the first 3 years of operations.

Date Asset Transaction Price

TZS

1 January 2018 Machines 1 and 2 Purchase @ 40,000,000

st

1 October 2019 Machines 3 and 4 Purchase @15,200,000

st

30 June 2020 Machine 3 Sale 12,640,000

th

1 July 2020 Machine 5 Purchase 20,000,000

st

Student’s Book Form Five

226

23/06/2024 17:36

ACCOUNTANCY_DUMMY_23 JUNE.indd 226

ACCOUNTANCY_DUMMY_23 JUNE.indd 226 23/06/2024 17:36