Page 74 - Book-keeping for Secondary Schools Student’s Book Form One

P. 74

Book-Keeping for Secondary Schools

reason, entries in the general journal should be focused towards a general ledger. In

other words, it is not common to find the general journal entry made in relation to an

individual account of a debtor or a creditor.

Functions of a general journal

A general journal has the following functions:

FOR ONLINE READING ONLY

(a) It acts as a diary where business transactions are recorded as soon as they occur.

(b) It gives the directions on which accounts should be debited and credited in respect

of each transaction, following the rules of double entry.

(c) It provides brief narrations of each transaction recorded. This is very important

because as opposed to the special journals, this journal records different types of

transactions.

(d) Since the transactions are recorded chronologically and include brief narrations, it

is easy for a person to review and identify any possible errors that may have been

made when recording.

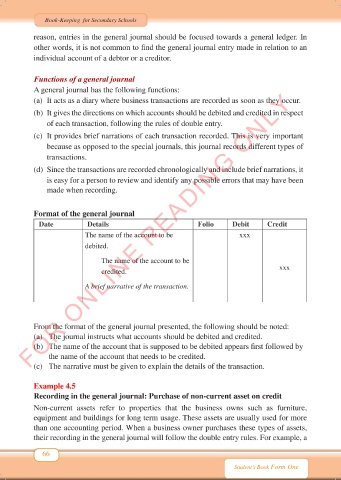

Format of the general journal

Date Details Folio Debit Credit

The name of the account to be xxx

debited.

The name of the account to be

credited. xxx

A brief narrative of the transaction.

From the format of the general journal presented, the following should be noted:

(a) The journal instructs what accounts should be debited and credited.

(b) The name of the account that is supposed to be debited appears first followed by

the name of the account that needs to be credited.

(c) The narrative must be given to explain the details of the transaction.

Example 4.5

Recording in the general journal: Purchase of non-current asset on credit

Non-current assets refer to properties that the business owns such as furniture,

equipment and buildings for long term usage. These assets are usually used for more

than one accounting period. When a business owner purchases these types of assets,

their recording in the general journal will follow the double entry rules. For example, a

66

Student’s Book Form One

Book Keeping Form 1 New 2024 FINAL.indd 66 18/10/2024 10:14