Page 222 - Accountancy_F5

P. 222

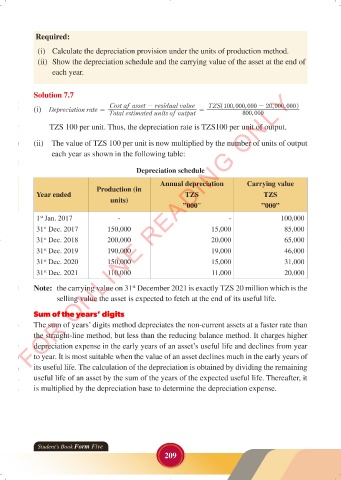

Required:

(i) Calculate the depreciation provision under the units of production method.

(ii) Show the depreciation schedule and the carrying value of the asset at the end of

each year.

FOR ONLINE READING ONLY

Solution 7.7

Cost af asset - residual value TZS 100 ,000 000 - 20 ,000 000h

,

,

^

(i) Depreciation rate = =

Total estimated units of output 800 ,000

LANGUAGE EDITING

TZS 100 per unit. Thus, the depreciation rate is TZS100 per unit of output.

LANGUAGE EDITING

(ii) The value of TZS 100 per unit is now multiplied by the number of units of output

each year as shown in the following table:

Depreciation schedule

Annual depreciation Carrying value

Production (in

Year ended TZS TZS

units)

”000” ”000”

1 Jan. 2017 - - 100,000

st

31 Dec. 2017 150,000 15,000 85,000

st

31 Dec. 2018 200,000 20,000 65,000

st

31 Dec. 2019 190,000 19,000 46,000

st

31 Dec. 2020 150,000 15,000 31,000

st

31 Dec. 2021 110,000 11,000 20,000

st

Note: the carrying value on 31 December 2021 is exactly TZS 20 million which is the

st

selling value the asset is expected to fetch at the end of its useful life.

Sum of the years’ digits

The sum of years’ digits method depreciates the non-current assets at a faster rate than

the straight-line method, but less than the reducing balance method. It charges higher

depreciation expense in the early years of an asset’s useful life and declines from year

to year. It is most suitable when the value of an asset declines much in the early years of

its useful life. The calculation of the depreciation is obtained by dividing the remaining

useful life of an asset by the sum of the years of the expected useful life. Thereafter, it

is multiplied by the depreciation base to determine the depreciation expense.

Student’s Book Form Five

209

23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 209 23/06/2024 17:35

ACCOUNTANCY_DUMMY_23 JUNE.indd 209